Financial services is like football—balance wins

Considering relationship services vs. transaction services

- |

- Written by Mike Moebs

- |

Important to proper planning and budgeting is an understanding of how relationship services can dilute fee income.

Relationship pricing, or sales, charges lower or no fees to gain new services. The service most likely impacted by a reduction in fee revenue is checking. This seems very fundamental, yet escapes much of the planning and budgeting done by banks, thrifts, and credit unions.

You have a relationship service when there are two or more services per account holder, and is usually achieved by cross-selling at the opening of a checking account. The checking account will be the fundamental service used for examples in this analysis.

A transaction service is where interchange and service charges are the biggest sources of revenue for the checking account.

The easiest way to measure a relationship, and the method where there is the most data available, is to take the number of services and divide by the number of customer or member accounts.

For all banks, thrifts, and credit unions this is 1.8 services per account holder. For banks, the average is 2.5 services per customer. Credit unions average 1.1 services per member.

For transaction services fee income-to-assets is a measure which is most readily available. Fee income-to-assets, or service charges-to-assets, annualized for all depositories in 2017 is 0.42%. For credit unions fee income to assets is 0.66%. Banks average 0.20% service charges to assets.

Using both measurements of cross-sell and fee income provides three important insights to relationships and transactions:

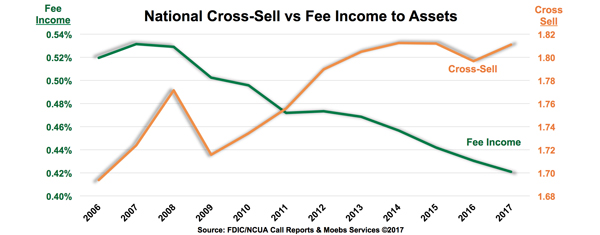

• Relationship services measuring by sales or pricing has gained with financial institutions over the past ten years. This has come at a loss of fee income—see the chart below.

• Banks are better than credit unions in cross-selling.

• Credit unions get more transaction fee income than banks.

Other factors in relationships and transaction services

There are several economic and market elements affecting relationship accounts and transaction accounts.

Following are the major things to consider:

• Free checking generates more transactions than any checking type. Free checking is used by 46.0% of the banks and 73.6% of the credit unions. Free checking often produces many transactions because it is the sole checking account for the entire family or household. Debit card and overdraft transactions generate fee income. If a depository offers free checking, this signals a transaction orientation. Those without free checking are usually relationship focused.

• Debit card transactions exceed cash transactions. As of the third quarter of 2017 debit card volume will be 29.3% of all payment channels transactions. Cash will be 28.6%.

The debit card is essential to the transaction business. Those financial institutions less than $10 billion assets earn more than 43 cents per debit card transaction, while those greater than $10 billion are limited by the Durbin Amendment of the Dodd-Frank Act to 25 cents.

Counter intuitively, smaller depositories have an incentive to be the peoples’ checking account, because they can make more revenue with unrestricted interchange yet offer free checking.

• Credit card revenue exceeds overdraft revenue. Overdraft revenue for years was well over half of service charges on deposits. In 2006, overdraft revenue represented 53.2% of fee income. In 2016 overdrafts represented $33.3 billion in revenue while credit card was $33.8 billion in interchange revenue. There are no Durbin Amendment restrictions on credit cards.

Combining the credit card and checking account achieves relationship services instead of standalone transaction services.

• Reward programs need to be financially effective. Reward programs earn points which can be redeemed for goods, services, and even financial services offerings.

Very large banks have extensive reward programs for credit cards which cost only about $1 per account because of the millions of people holding credit cards with the bank. Couple this low-cost reward program with an interchange amount per transaction which is almost four times as much as the Durbin Amendment restriction on big bank debit card interchange, and the strategy of reward program for credit card is financially sound.

Depositories under $10 billion in assets cannot compete with the large banks because of their small number of credit card users. Smaller depositories can compete on debit cards where the price restriction only applies for large banks.

What football can teach bankers

Some financial institutions view checking needs to be either relationship or transaction oriented. The best answer to this is an analogy.

How many football teams have won the Super Bowl by being one-dimensional: run or pass?

None.

The answer is the same for relationship services and transaction service—balance wins.

7 steps to start with

The following are guidelines for both relationship and transaction services:

1. Offer both relationship-oriented and transaction-oriented services. Or, offer two checking accounts.

2. Free checking drives transactions.

3. In relationship services checking does not have to be the primary financial service. Other financial services can be primary and a no-charge checking account seals the relationship.

4. Debit card is the primary feature of checking. Being able to provide a replacement card in 24 hours or less is essential.

5. Credit card reward programs are not for depositories less than $10 billion in assets.

6. Financial institutions less than $10 billion can use debit card reward programs as long as the Durbin Amendment exists.

7. Both relationship and transaction services need to be profitable. The days of loss leader financial services is over.

Semper,

Mike Moebs

(Mike will respond to questions at [email protected])

Two articles supporting this blog by Banking Exchange Contributing Editor Melanie Scarborough are:

Tagged under Blogs, Big Data, Fee Income, The Prairie Economist, Mergers Acquisitions, Lines of Business,

Related items

- UBS Expands US Banking Push for Affluent Wealth Clients

- Why most European challenger banks fail in the US — and where the real opportunity lies

- Securitize Set for NYSE Debut Following SPAC Merger Approval

- Colony Bankcorp Agrees $163m First Reliance Deal

- Cross River and Fireblocks Discuss How to Build and Scale Products