What's left on your HTM bucket list?

SNL Report: Banks continue to build HTM portfolios while rates remain low

- |

- Written by SNL Financial

By Nathan Stovall and Salman Aleem Khan, SNL Financial staff writers

Banks continued to build their held-to-maturity securities portfolios to protect against rising interest rates, but growth slowed as institutions neared full compliance with regulations that influenced them to seek safety from swings in the market.

As interest rates remained low and banks faced new capital and liquidity standards in recent years, they placed large amounts of securities in held-to-maturity (HTM) portfolios. Unlike available-for-sale (AFS) portfolios, banks are not required to make mark-to-market adjustments to their HTM buckets on a quarterly basis.

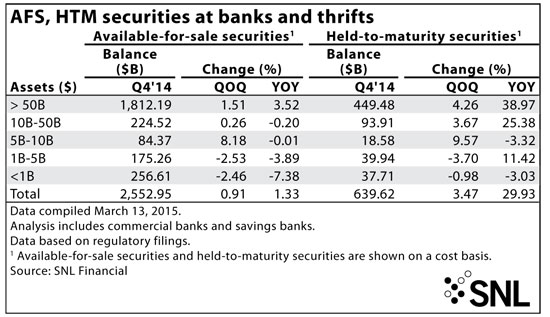

Those mark-to-market adjustments in AFS portfolios flow through accumulative other comprehensive income, or AOCI, and impact tangible common equity. Banks have sought to mitigate the impact of changes in market valuations on their book values by relying on their HTM portfolios more and more. Banks increased their HTM portfolios to 20.05% of all securities at the end of the fourth quarter from 19.65% in the linked quarter and 16.36% a year earlier, according to SNL data.

For a larger version, click on the image.

For a larger version, click on the image.

Impact of LCR standards

Banks have classified as HTM a number of liquid securities purchased to meet the requirements of new provisions such as the liquidity coverage ratio (LCR) since those bonds are likely to come under pressure when interest rates rise. Banks with more than $250 billion in assets began complying with the LCR on Jan. 1, 2015, and spent much of the first nine months of 2014 working toward compliance with the provision. As those institutions built "high-quality liquid assets" such as U.S. Treasurys that they are required to hold under the LCR, they placed many of those securities in their HTM portfolios.

SNL data show that banks reported a 78.12% sequential increase in the amount of U.S. Treasurys held in HTM portfolios in the fourth quarter, and an increase in excess of 60% in the second and third quarters of 2014.

For a larger version, click on the image.

For a larger version, click on the image.

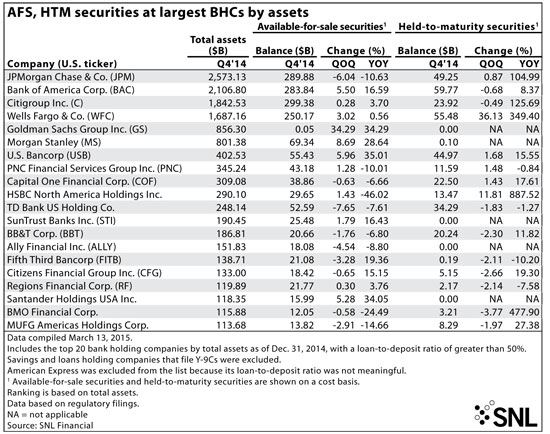

Larger banks that have to comply with the LCR have led the way in building HTM portfolios over the last year. Not only are large banks trying to protect those bonds from swings in the market, but under the Basel III rules, changes in the value of AFS portfolios would also flow through regulatory capital at institutions with more than $250 billion in assets.

Banks with more than $250 billion in assets—JPMorgan Chase & Co., Bank of America Corp., Citigroup Inc. Wells Fargo & Co., Goldman Sachs Group Inc., Morgan Stanley, U.S. Bancorp, PNC Financial Services Group Inc., Capital One Financial Corp. and HSBC North America Holdings Inc.—increased their HTM portfolios in the fourth quarter by a median of 1.46% from the prior quarter, but grew those portfolios by more than 60% from a year earlier, according to SNL data.

Banks with more than $50 billion in assets—which are subject to the LCR—have built their HTM portfolios considerably as well. Banks in that group increased their HTM portfolios at the end of the fourth quarter by 4.26% from the linked quarter and 38.97% from year-ago levels.

Smaller institutions’ strategies more muted

Smaller banks have relied on their HTM portfolios, as well, though the increases have been far less pronounced than their larger counterparts and growth continued to slow in the fourth quarter.

Banks between $1 billion and $5 billion in assets decreased their HTM portfolios in the fourth quarter, while other institutions between $1 billion and $50 billion in assets continued to build their HTM portfolios in the period. Overall, that group of institutions built their HTM portfolios in the fourth quarter by 2.29% from the linked quarter.

SNL found that banks with less than $50 billion in assets decreased the size of their AFS portfolios from year-ago levels. Institutions below the $50 billion asset threshold reported mixed growth trends in their AFS portfolios from the linked quarter as banks with less than $5 billion in assets shrunk those portfolios, while banks with assets between $5 billion and $50 billion reported modest linked-quarter growth in their AFS portfolio in the fourth quarter.

For a larger version, click on the image.

For a larger version, click on the image.

Yet AFS continues to dominate

The vast majority of the banking industry's securities still remain in the bucket that is subject to changes in market values. Banks show those changes in values, and whether they have recognized gains or losses, by disclosing the level of unrealized gains and losses in their AFS portfolios every quarter. When long-term rates rose in 2013, the level of unrealized gains in bank portfolios nearly erased.

Long-term rates actually fell in the fourth quarter and have continued to fall in 2015 despite the expectations that rates will at some point move higher. The yield on the five-year Treasury declined by 25 basis points and the 10-year Treasury yield fell by 35 basis points in the fourth quarter.

Long-term rates have fallen further since the fourth quarter closed, with the yields on the five-year and 10-year each declining by more than 20 basis points. While long-term rates have fluctuated in 2015, the long end of the yield curve fell last week after the Federal Reserve extended many market watchers' expectations for a rate increase beyond midyear. As the market's expectations for higher rates moved out further on the time horizon, long-term rates fell back down to low levels.

"That post-FOMC trade, recall, featured a big reduction in the market-implied probability of a June rate hike and declines in yields on the long end based on expectations of a lower peak fed funds rate," Janney Montgomery Scott noted in its daily fixed income commentary on March.

Tagged under ALCO; Mergers Acquisitions; Financial Trends; Feature; Feature3;

Related items

- Global Instability and Rising Treasury Yields, but Markets Open Higher

- “Stablecoin Strategy” Is a 2026 Question for Banks, Not a 2027 One

- Banks Need to Reconsider their Role in an AI-Driven Future

- Tokenization Could Reshape Financial Markets, Says IMF

- UBS Expands US Banking Push for Affluent Wealth Clients