Checking customers not created equal

Half of accounts unprofitable, only 10% "lucrative"

- |

- Written by Lisa Arnold

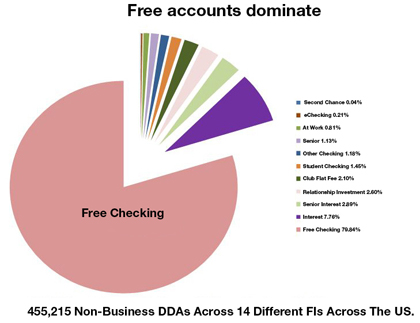

In a survey, Affinion Group found that while institutions offer a wide variety of non-business checking account options, nearly 80% of actual accounts are one form or another of free checking. Click here or on the image for a larger version.

Larger financial institutions have tried to charge new fees, with varying degrees of success. Regardless, today, about 80% of all checking accounts among banks and credit unions of less than $5B in asset size still predominately offer free checking.

After reviewing over 450,000 DDAs from 14 different financial institutions across the US, results show the average DDA's monthly contribution to revenues generated (less variable costs) looks promising, at about $25 per month.

But that's misleading.

When we start digging into the individual DDAs included in the review, we see some troubling realities. Instead of looking at the average, take a look at the median individual revenue generated by these 450,000. Then we see the revenue generation closer to about $2.50/month.

Odd as it may sound, a bank's highest-value customers are typically worth so much to the bank that they're skewing the banks' overall numbers.

Click here or on the image for a larger version.

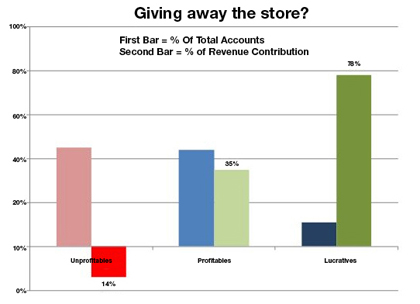

Statistics indicate that typical institutions have three types of checking account customers within their banking family.:

• Unprofitable accounts: Customers who are not generating enough revenue to cover variable costs.

• Profitable accounts: Customers who are covering variable expenses plus generating moderate revenues.

• Lucrative accounts: Customers who are generating a significant revenue for the financial institution.

Examining unprofitable accounts

About 45% of all DDAs in the review, which we'll treat as our universe for this article's analysis, lose money. (This considers revenues generated minus variable costs.) These are accounts that don't have much on deposit and which are not utilizing cost efficient/revenue-generating alternatives--for example, they are still writing paper checks and not actively using a debit card.

This 45% is costing the bank about 14% of the total revenues generated by all DDA accounts. Adding fixed costs into this equation makes the loss is even worse.

Of course, as was mentioned before, using the mean can skew data, and you can't assume that each 3% of total accounts that is unprofitable is equal to 1% of revenue lost. Further below, we'll address a few ways that you can address the different levels of "unprofitable accounts."

Examining profitable accounts

Another 44% of DDAs generate some positive revenues, or enough to cover variable expenses plus moderate revenues. These customers have somewhat higher balances than those customers who are Unprofitable Accounts, and are typically using a debit card fairly regularly.

The goal with these customers should be to encourage more profitable/paperless alternatives (e-Statements, direct deposit, more debit card usage, etc.). There are clear behavior patterns that can be leveraged to increase the profitability of these accounts.

For example, our research indicates that about a third of "Profitable Account" holders are using paper statements, as opposed to online statements. If you consider all of the costs associated with paper statements, (from printing to postage), you come up to around $1 per month, per customer that a bank needs to spend on these statements (or $12 per year). Multiplied out across your customer base, eliminating that cost would be a significant boost to your bottle line.

Paper statements are just one of many customer behaviors that hinder accounts from being more profitable. Thorough analysis of these characteristics can reveal significant opportunities for financial institutions to improve profitability without the need for fees.

Lucrative accounts--a model to build on

The remaining 11% of DDAs generates nearly 78% of your total Checking Account Non-Interest Income. A typical "Lucrative Account" generates about $130/month per account.

Identifying the types of account holders may yield surprising results. A large piece of your revenues are coming from fees and interchange. Only about 10% of "Lucrative Accounts" carry significant balances. Whereas, the remaining 90% of a typical institution's "Lucrative Accounts" generate serious revenues via interchange and NSF fees.

Unlike the aforementioned "Unprofitable" and "Profitable" accounts, these "Lucrative Accounts" must be protected.

Finding, keeping, and building on your lucratives

All customers are not created equal:

Small group feeds your bottom line. The typical rule of business is that 80% of income comes from the top 20% of customers. Based on actual numbers, we're finding that the banking industry leans more extreme than expected. Almost 80% of a bank's revenue is coming from 11% of their customers.

Balances aren't the profit point. Of the 11% mentioned, only about 2% have a balance that generates significant income, and the other 9% are generating just as much profit as your high-end depositors. This income source is related to profitable behavior.

Who covers your costs. About 44 of every 100 customers are generating revenue that will cover variable expenses.

Who's costing you. About 45 of every 100 customers are costing financial institutions, about $33 per month.

In the face of regulatory scrutiny, bankers must consider what makes up "Lucrative Accounts" and "Profitable Accounts," and create account requirements accordingly. The goals are to protect the profitable behavior of "Lucrative Accounts," grow the "Profitable Accounts" into "Lucrative Accounts," and identify ways to move "Unprofitable Accounts" into the "Profitable Account" category.

How to find profitability in unprofitable accounts

To accomplish such tasks, banks must re-think some typical approaches:

1. Learn to ignore some squeaky wheels. In some cases, the worst offenders are particularly difficult to deal with in regards to the bottom line. One of the key challenges to this group is that many of these accounts tend to have both a negative balance and an overwhelming amount of NSF refunding, meaning that banks are losing twice with these accounts. "Life happens" to every bank customer, but the key challenge for banks with the "worst offenders" in the "Unprofitable Account" category is not to refund automatically every time a customer asks, but instead to identify which customers fall into the "this is occasional" category or which fall into the "this is a pattern" category.

Banks should make the decision on waiving fees or not based on the value of the banking relationship, not the squeaky wheel.

2. Don't bother with rules you won't enforce. Many banks have tried to address these customers by placing restrictions on these types of accounts, with some impact. However, our research indicates that banks aren't necessarily enforcing the restrictions.

In some cases, more than two-thirds of account holders with restrictions aren't living up to their end of the bargain.

3. Consider incentives, not just penalties. In the case of enforcing restrictions on an account, we believe many banks are only getting it half correct (even those with a high percentage of profitable customers). We're all familiar with the carrot and the stick, and unfortunately, only the latter is showing up in these types of situations.

We've seen that customers are willing to change behaviors for certain rewards, and recommend aggressive carrot and stick models to address "Unprofitable Accounts."

However, like the full spectrum of bank accounts, not all "Unprofitable Accounts" are created equally. In fact, some of our partners have identified this type of account as a built-in opportunity to grow their account base. Second-chance-checking programs, or pre-paid card programs, can allow a financial institution to educate consumers on how to successfully maintain a bank account, ultimately leading to "Profitable Accounts."

About the author

|

Lisa Arnold is a Marketing Analyst with Affinion Group, a leading provider of ancillary services to financial institutions. For more information, visit Affinion.com.

Tagged under Mergers Acquisitions; Big Data;