Spending in a Pandemic: A New Look at Changing Consumer Behaviors

The COVID-19 pandemic has upended virtually every aspect of life for American consumers

- |

- Written by Linda Turnbull, Associate Managing Director at Argus Information and Advisory Services

Introduction

The COVID-19 pandemic has upended virtually every aspect of life for American consumers, from how we engage socially and how we work to how we shop and play. Not surprisingly, consumer spend behaviors changed in important ways as well. Understanding these changes is central to building effective strategies going forward. To this end, we studied broad spend dynamics across the consumer wallet via a novel dataset. Our initial questions asked how consumer spend changed during the pandemic along three primary dimensions:

- Level — How much did the amount consumers spend change?

- Type — What did they spend on?

- Instrument — What did they use to spend?

In addition to these questions on past performance, we also explored spend recovery. Specifically, has recovery begun yet? If so, when did it begin and how is it progressing? If spend recovery is not yet complete, when might we expect it to be so? Of course, a study of this magnitude and complexity requires a very special dataset.

The Analytical Dataset

Analyzing spend at the individual consumer level is a challenge. The primary difficulty is that no single institution has access to all channels of consumer spend. Consider that credit card issuers can see every transaction on their own cards but do not see those of their competitors. The same is true for processor networks. Beyond issuers and network processors, transaction volumes are increasing via alternative channels (e.g., Venmo, Zelle, Cash App, PayPal, etc.), which pose a universal insight gap for traditional issuers, networks, and data aggregators alike. Of course, it remains impossible to track pure cash transactions.

To overcome these challenges, Verisk Financial built a dataset comprised of 20 million anonymized consumers selected via stratified random sampling from among those consumers for whom Verisk Financial has both credit and debit transaction data. These 20 million consumers match the joint distribution of all credit card users in the US by credit risk tier, age, geography, and Q4 2018 aggregate credit card balance.

In total, our analytical dataset includes 12.4 billion credit and debit card transactions. While not the final word, analysis of this dataset affords perhaps the most comprehensive exploration of spend during the pandemic available today.

Results

Level of Spend

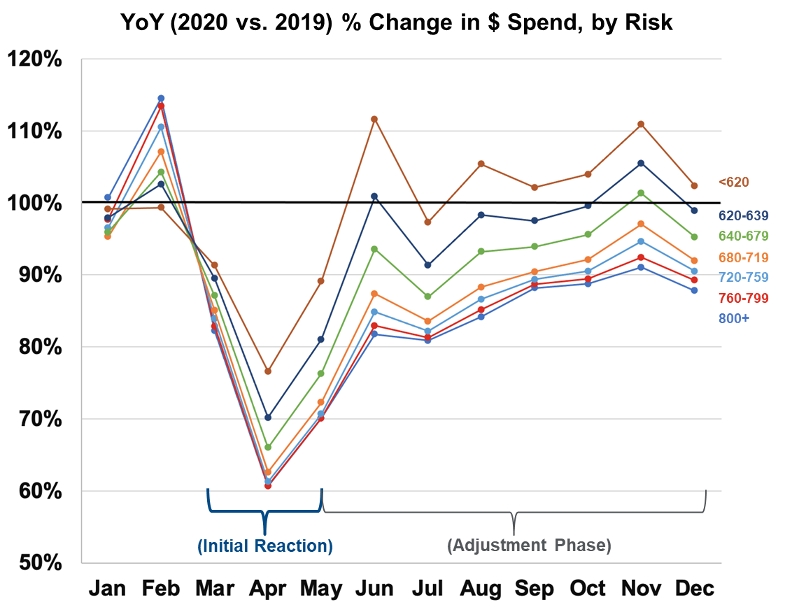

Figure 1 shows the year-over-year trend in overall consumer spending levels for 2020. This approach allows us to control for seasonality. There are three important aspects of this graph. The first is the trend: a significant drop in spend in March, when business shut down broadly across the country, followed by an even more severe drop in April. However, spend immediately began to recover in May 2020. That recovery has been relatively stable and consistent since it began. The expeditious onset of spend recovery in this pandemic is a marked departure from the recovery experience of the 2008 recession, where lower spend and changes in payment prioritizations lingered for months.

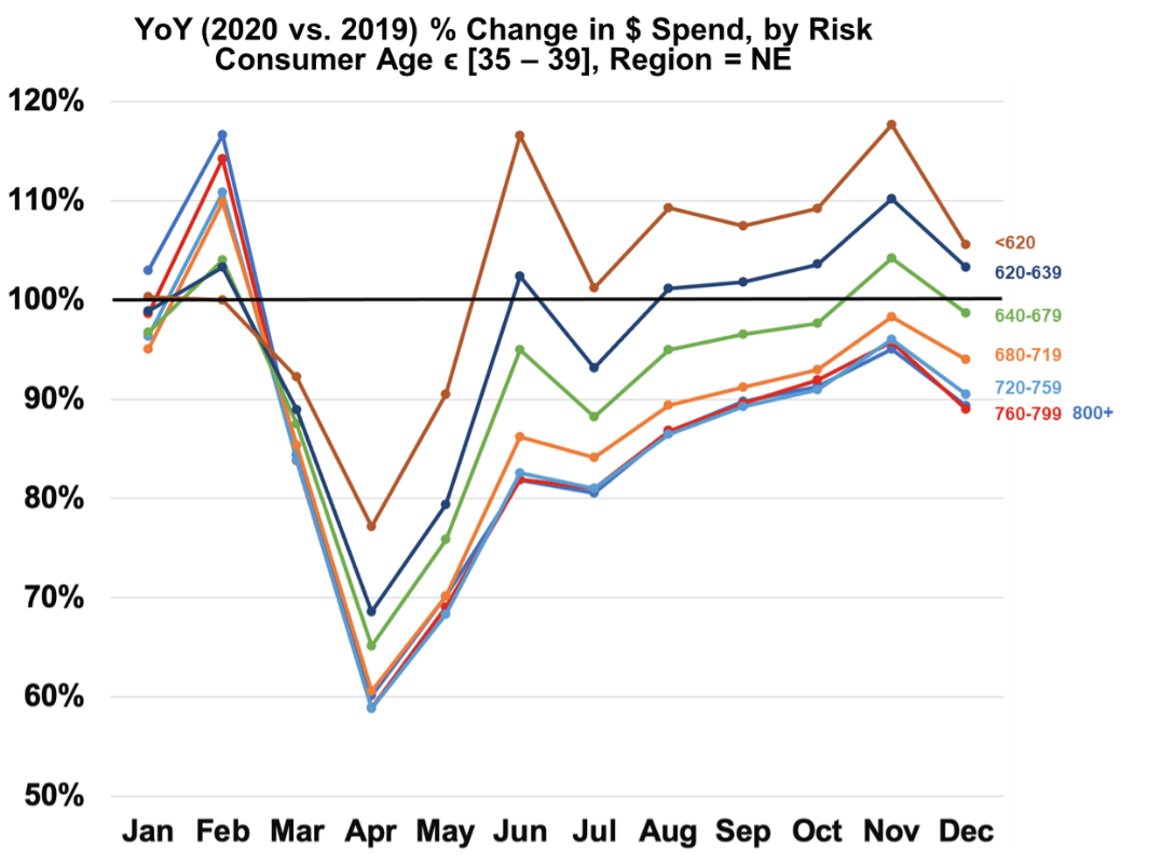

Second point: this trend of an initially severe but short-lived shock, followed immediately by the onset of recovery was remarkably consistent across every view of the data. To illustrate, Figure 2 shows the same trend for consumers aged 35 to 39 in the Northeast region of the country. In no other analysis have we seen such a consistent response dynamic.

We believe there are several explanations for this consistency. First, the national shutdown in March and April 2020 likely was a driver of the uniform initial pullback in spend. Also, national media attention on the pandemic probably contributed to this first reaction. In terms of the speed of recovery onset, we suspect robust online and digital shopping options allowed consumers to adjust quickly to distance and contactless transactions (consider Instacart, UberEats, Grubhub, etc.). Factoring in the speed with which people adjusted to remote work along with the availability of government stimulus programs, we believe the data speak to an environment that fostered remarkable resilience among consumers.

The third noteworthy insight in these graphs is the counter-intuitive rank-ordering of the pull-back in spend by credit-risk tier. The conventional wisdom is that lower-risk consumers generally have more disposable income, and hence should have more wherewithal to recover quickly. In fact, the opposite was true. More on this result later in this article.

Type of Spend: Essential vs. Non-essential

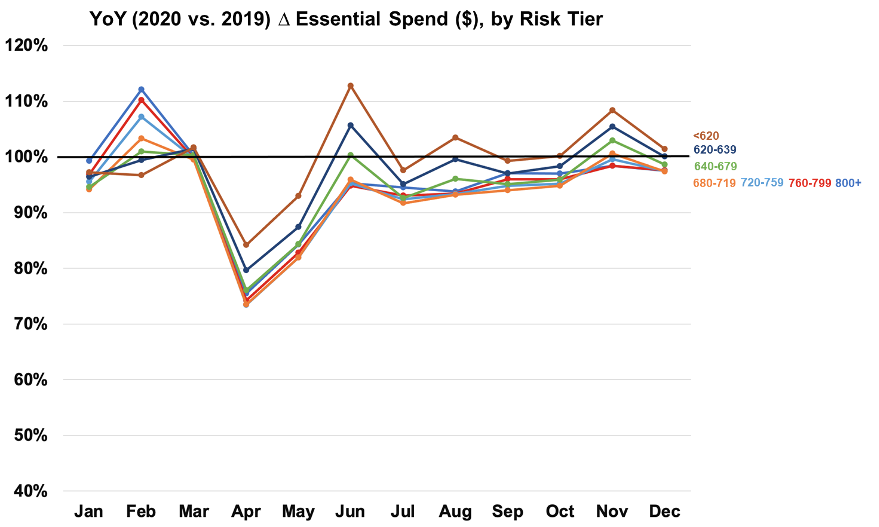

Figure 3 shows the year-over-year trends in essential spending, i.e., for things considered to be fundamental to ongoing health, safety, and wellness. Note the speedy recovery across the risk spectrum. By the end of 2020, nearly every risk tier had either fully recovered in essential spend or was nearly fully recovered.

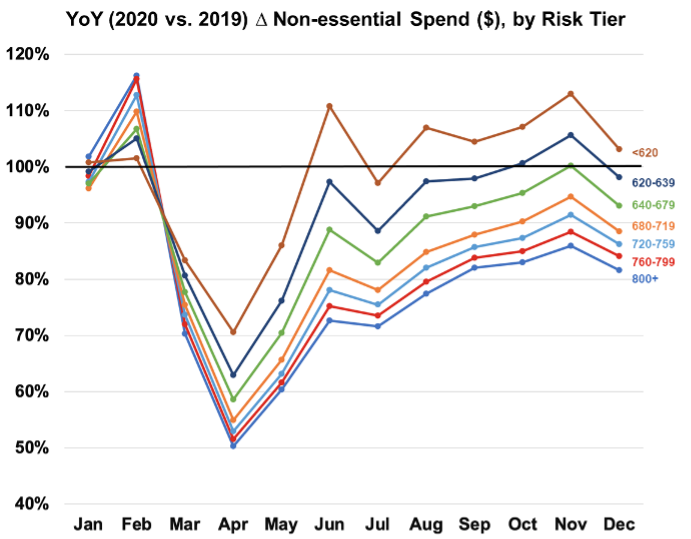

Figure 4 shows the same basic pattern for non-essential spend, although the drop in March and April was more severe, and the recovery slower.

There are several possible drivers of this behavior. The first is that the nature of non-essential spend differs by risk tier. For example, travel comprised 24% of pre-pandemic non-essential spend for lower-risk consumers, but only 17% for higher-risk consumers. So, while consumers might have felt more comfortable in the second half of 2020 eating at an outdoor restaurant, they may not yet have felt comfortable boarding an airplane. Consumer comfort with various non-essential activities is not uniform, and their spend will reflect that fact.

Another potential driver of slower recovery in non-essential spend among lower-risk consumers is that recovery in this group requires more transactions and more spend. For example, consider consumers between the ages of 30 and 34 living in the Midwest. Those with credit scores between 620 and 639 had on average only five fewer non-essential transactions in 2020 compared to 2019, for an average drop of only $68. That amount could be made up in one additional restaurant meal. In contrast, those with credit scores between 720 and 759 had 12 fewer non-essential transactions, but with an average drop of $1,285. The point is clear: lower-risk consumers had more non-essential spend to make up to recover fully, and may still be uncomfortable with some of the non-essential spend categories they had favored pre-pandemic. These results imply that full spend recovery will not occur until non-essential spend has recovered among the lowest-risk consumers.

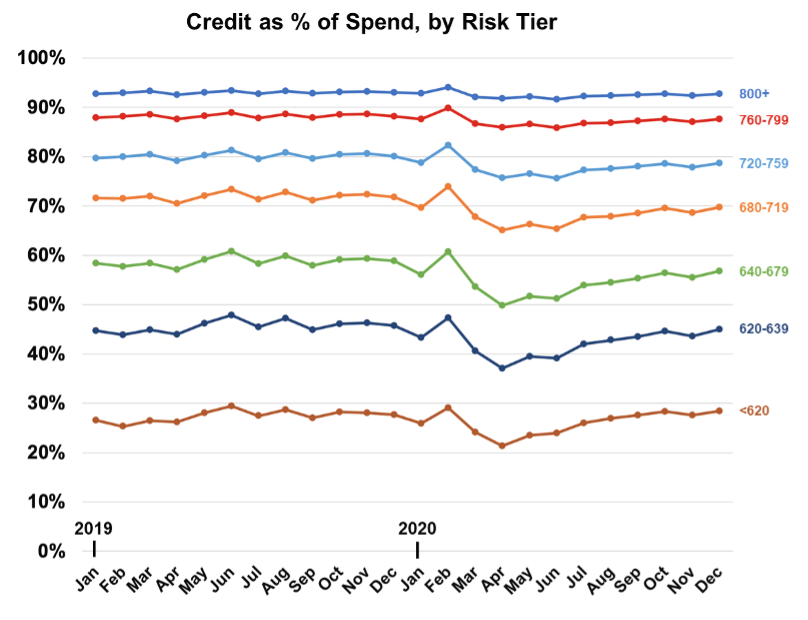

Instrument of Spend: Credit vs. Debit

The initial drop in the percentage of credit spend in March and April of 2020 (Figure 5) was more pronounced for higher-risk consumers. This dynamic is due in part to lower-risk consumers having significantly more credit available to them, so they face less pressure to conserve credit in uncertain times. Another driver is government stimulus; higher-risk consumers were more likely to shift toward debit spending to access those funds. In any case, this effect was short-lived; credit spend as a percentage of overall spend had more-or-less fully recovered by December 2020.

Recovery Analysis

Recovery began in May of 2020 with remarkable consistency. Essential spend had more-or-less fully recovered by the end of 2020, as had the proportion of usage of credit versus debit. The remaining factor in achieving full spend recovery, therefore, is the recovery in non-essential spend.

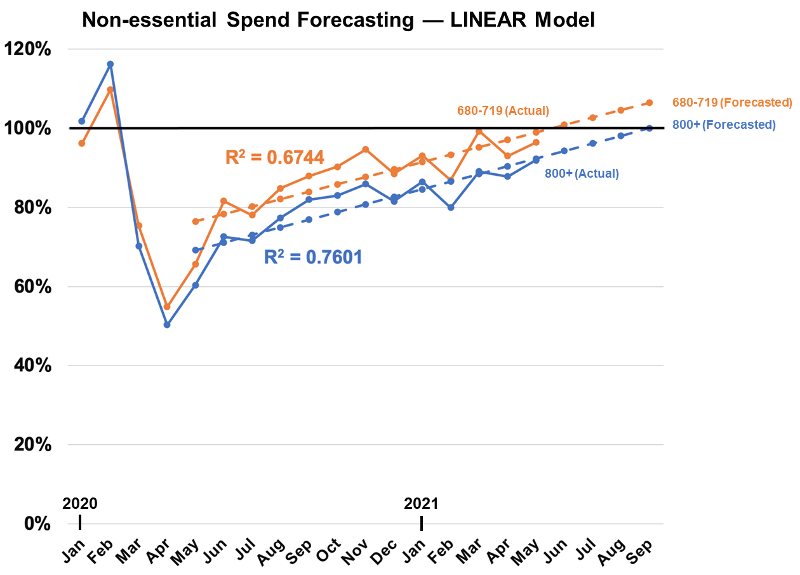

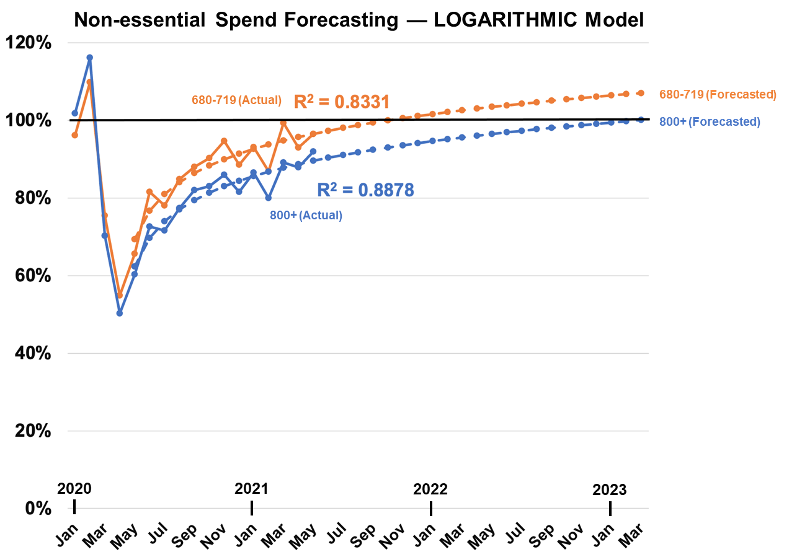

To estimate when non-essential spend will recover (and hence when spend overall will recover), we built simple linear and logarithmic models (Figures 6 and 7, respectively) based on non-essential spend by risk tier from May 2020 through May 2021.

We tend to lean toward the more conservative logarithmic model, expecting full spend recovery sometime in late 2022 or early 2023. Our perspective is informed in part by the fact that the pandemic is far from over; Delta and other variants continue to cause uncertainty in the marketplace.

The drop in spend during the pandemic suggests that “on-us/off-us” spend analysis would be a particularly useful exercise in the near-term. As consumers return to pre-pandemic spend levels, they may choose to do so with different cards than they used previously. Transitional periods are also opportune times to evaluate marketing strategies; what may have been effective with certain market segments before the pandemic may be less so now, and vice-versa. This may be particularly salient given the many counter-intuitive behaviors we found through this analysis.

Summary

Spend analysis at the consumer level is challenging. This study provides several significant insights into consumer behavior during the pandemic. While some of these behaviors confirm conventional wisdom, others force us to reconsider our notions of the consumer mindset. We have also discussed how strong technologies and merchant innovations can influence spend behaviors. Beyond the significant value of these insights, the results suggest several strategies for issuers to explore. Those who understand not only how consumer spend preferences are changing, but also the right engagement approach in this transitional period, will be in a much stronger position to gain market share and build long-term relationships with their respective customer bases going forward.

Author: Linda Turnbull, Associate Managing Director at Argus Information and Advisory Services

Tagged under Retail Banking, Financial Trends, Feature, Lines of Business, Technology, Social Media, People, Customers, Revenue, Mobile, Online, Cards, Consumer Compliance, Feature3, Big Data,

Related items

- Inflation Continues to Grow Impacting All Parts of the Economy

- Banking Exchange Hosts Expert on Lending Regulatory Compliance

- Merger & Acquisition Round Up: MidFirst Bank, Provident

- FinCEN Underestimates Time Required to File Suspicious Activity Report

- Retirement Planning Creates Discord Among Couples