Banks must speed b2b pay integration

Reports note disconnect between corporates and banks over use of “integrated receivables”

- |

- Written by Bill Streeter

Checks may be “old school,” but for corporate receivables, they're easier to deal with than matching an incoming ACH with an e-mailed remittance.

Checks may be “old school,” but for corporate receivables, they're easier to deal with than matching an incoming ACH with an e-mailed remittance.

A pair of related research reports from Aite Group point to an ironic twist in the world of corporate payments: Check-based payments, still the largest category of b2b payments, though declining, is actually more efficient than electronic payments.

Decades of fine-tuning of wholesale lockbox software and procedures have set a fairly high bar for efficiency and data integration for check payments. So much so that even though electronic payments are quicker and more certain of delivery, their straight-through processing (STP) rates are low by comparison to checks.

In her report, The Corporate Need for Integrated Receivables, Aite Senior Wholesale Banking Analyst Erika Baumann writes:

“With the rise of electronic payments, automated matching of remittance information to automate the cash application process sees a sharp decline. Low STP rates of electronic payments is creating a new need for corporations to replicate the efficiencies in paper check processing via lockbox for electronic payment types.”

Money in one door, remittances another

More than 50% of corporations receive at least a quarter of their payments from other corporations as an ACH payment, according to the Aite Group survey. Baumann says NACHA data indicate that 61% of automated clearing house payments “send remittance information separately from the payment, most commonly by email.” This results in manual work for corporations. Baumann’s report, based on a survey of treasury professionals at 145 U.S.-based corporations, notes that one-third of respondents say that better tools could eliminate more than half, or even all, of their electronic payment exceptions.

Meaning of “Integrated Receivables”

In a companion report, Banks Journey Into Integrated Receivables: A Three-Pronged Approach, by Christine Barry, research director of Aite’s Wholesale Payments Group, the term “integrated receivables” is described this way:

“The ability to receive any type of payment from any channel, in any format, and be able to present it back to the customer in a consolidated report.” Such a system allows remittance information to accompany electronic payments and standardizes the file formats to make incoming payments and data easier to upload into corporate data systems.

The report identifies vendors that provide one or more components of integrated receivables. These companies were the ones mentioned most often by bank respondents: Deluxe Treasury Management Solutions, HighRadius, ImageScan, Paybox, US Dataworks, Transcentra, and VersaPay.

Baumann, in an interview, notes that these companies typically will work with banks or with corporations directly.

Corporates ahead of banks

The message from both reports is clear: the banks that predominantly operate in the wholesale lockbox space need to up their game or risk losing business to nonbank players.

Just over half of the treasury professionals surveyed report that they plan to invest in—or have already invested in—an integrated receivables solution. Forty-four percent of those planning to say theywill make this move within the next 6 to 12 months.

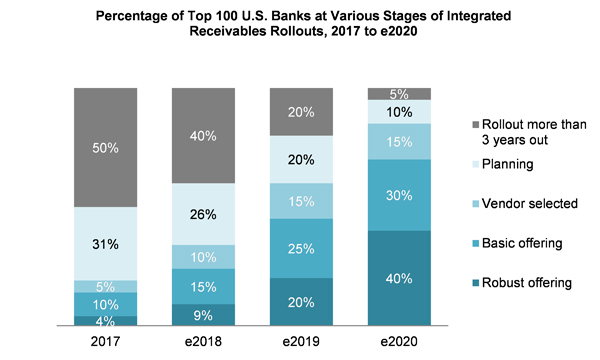

By contrast, banks’ plans are not as far along overall. Aite reports that only a handful of the top 100 U.S. already have such an offering. Two thirds of these banks are still in the planning stages or three years away from a rollout (see chart, below).

Source: Aite Group

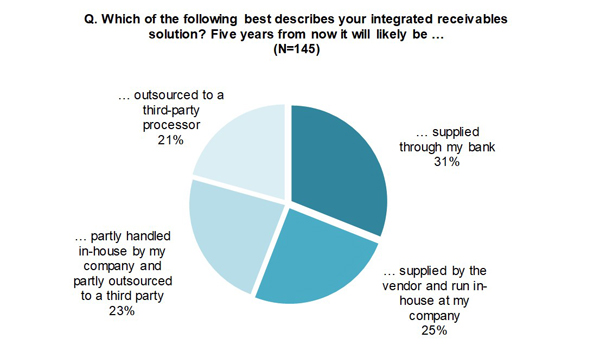

If this disconnect continues, banks may lose out on the opportunity to be the provider of an integrated receivable system. Indeed, Aite reports that only 31% of corporate treasury professionals say they anticipate partnering with their bank for this solution (see chart, below).

Source: Aite Group

Opportunity cost

Baumann observes that by not helping corporate client integrate receivables, banks would face a potential loss of fee income. More significantly, they would forfeit an opportunity to tie in a corporate customer more closely. Baumann says that both lockbox and integrated receivables services are very “sticky.”

She also points out that creating a more efficient means to handle electronic payments by the payee becomes even more important once real-time payments come into effect more broadly.

“It’s all fine and well to get your payment within a minute,” Baumann observes, “but if you can’t apply that payment, what good has it really done you?”

Banks preferred, but only for so long

Baumann has worked both on the sales side at a bank technology vendor and at a large bank. She believes corporates still want to partner with a bank for an integrated receivables program. One reason why, she says, is that they recognize there would be fewer integration issues. However, the problems of mismatched electronic payments and invoices is big enough thorn that corporations will work with anyone that can provide a solution, says Baumann.

A handful of the largest banks are investing significant funds in this area (Aite estimates the initial spend at the top four banks at $4.5 million, with a couple of them indicating they will spend far more.) Bank of America, Baumann notes, is partnering with fintech provider HighRadius.

The giant bank announced last August that it was rolling out what it calls “Intelligent Receivables,” to help companies improve their “straight-through reconciliation.”

Related items

- Global Instability and Rising Treasury Yields, but Markets Open Higher

- “Stablecoin Strategy” Is a 2026 Question for Banks, Not a 2027 One

- Banks Need to Reconsider their Role in an AI-Driven Future

- Tokenization Could Reshape Financial Markets, Says IMF

- UBS Expands US Banking Push for Affluent Wealth Clients