Time to adjust your sails?

Key considerations for your 2017 budget

- |

- Written by ALCO Beat

ALCO Beat articles featured exclusively on bankingexchange.com are written by the asset-liability management experts at Darling Consulting Group.

ALCO Beat articles featured exclusively on bankingexchange.com are written by the asset-liability management experts at Darling Consulting Group.

"The pessimist complains about the wind; the optimist expects it to change; the realist adjusts the sails."—William Arthur Ward

By Vinny Clevenger, managing director, Darling Consulting Group

As most in New England would attest, the weather plays a constant role in our lives. This is even more relevant for those of us who enjoy spending time on the water.

Weather dictates the rhythm of our lives. What is the speed and direction of the wind? How big is the swell? Is the sun staying out all day? What times are the tide changes? Will the fog lift by noon?

On and on it goes—a never-ending cycle of monitoring the weather and planning for the best possible utilization of our precious time.

Ward's quote reminds me of the various members at our marina. After numerous trips, we arrive back at the dock and I'm always amused by the variety of reasons for staying in port.

In that sense, it's a very similar experience when discussing budgeting with banking executives across the country.

Those who fell short of expectations during 2016 are prone to blame idiosyncratic factors which may have influenced their results. Conversely, others may contend that conditions are destined to improve. They hope their fortunes will recover accordingly.

I hope that the prevailing winds were beneficial to your organization during 2016. Nonetheless, it is a time to reassess the direction of the organization and forecast future conditions.

While no one expects smooth sailing, careful consideration of the following key issues will help you weather the forthcoming year.

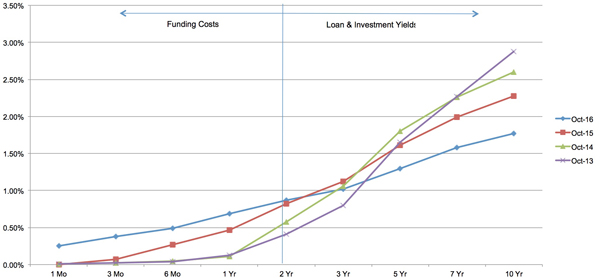

1. Interest Rate Forecast

If nothing else, the wind direction has been relatively constant for the majority of 2016.

The Federal Open Market Committee had prognosticated four future interest rate increases and the 10-year U.S. Treasury started the year at 2.24%. However, in the event, the FOMC has stood pat—through the November meeting—while the 10-year Treasury rallied and has subsequently settled into a narrow trading range since the summer.

So instead of getting a rising rate scenario which many had embedded into their forecasts, we got a "flattening" falling interest rate environment.

So where do we go from here?

Click on the image for a larger version.

Click on the image for a larger version.

Many folks are comfortable forecasting one or two additional moves from the FOMC during 2017 but believe the longer end of the yield curve may remain relatively unchanged from current levels. This translates to a "flattening" rising rate scenario.

History suggests this could be the case. The last five tightening cycles by the FOMC have resulted in the 2-10 spread reaching 0 basis point (or perhaps negative) at some point during the cycle.

Maybe this is the year.

Or maybe not.

No matter what the future holds, there will be significant variances between a forecast of higher rates with a parallel or steepening yield curve versus higher rates with a flattening yield curve.

One of the most common missteps in 2016 was the over-forecasting of loan yields, which resulted in a shortfall of net interest income. The key is to understand how the potential future shape of the yield curve influences your business and to forecast appropriately.

2. Asset Growth Assumptions

Although industry data suggests that net interest margins (3.57%) were unchanged through the initial two quarters of the year (see FDIC's June Quarterly Banking Performance review), this is because most institutions have continued to alter the mix of their balance sheet away from investments and into loans.

But how much longer can this game last?

Click on the image for a larger version.

Click on the image for a larger version.

With liquidity tightening, hyper-competitive loan pricing, floored deposit costs, and a potentially flatter yield curve on the horizon, how will financial institutions offset this duress in 2017?

Loan growth emerges as the primary solution to this dilemma. But how much additional incremental loan growth will a balance sheet need to replicate the interest income generated during 2016?

In other words, if you grew loans by 3% during 2016, does that figure need to be increased to 4%-6% for the 2017 forecast?

What are your expectations for prepayment? Additionally, what impact could this have on the liquidity profile of the organization? If your loan/asset ratio is meaningfully rising, is management and the board comfortable with the organization's ability to fund unforeseen deposit runoff?

Further complicating matters is the regulatory perspective on commercial loan concentrations. If your organization has added a significant amount of commercial loans over the past several years, or has a portfolio of these loans around three times your capital position, you can be certain that your regulator has taken notice. Will this incremental loan growth compromise your organization's policies or solicit additional scrutiny?

If your balance sheet can still comfortably "shift" the mix from investments into loans, it is important to understand how much additional growth is necessary to reach your targets. Conversely, others who have been playing that game for the past several years are starting to plan for additional security purchases in the upcoming year.

3. Deposit/funding strategy

A large unknown for banks is the behavior of their deposit base as rates increase.

In the wake of the financial crisis, deposit growth surged at many organizations. To date, most of those dollars still reside on balance sheets across the country.

One school of thought is that they are awaiting an opportunity for better returns.

The counter argument is that these are truly core deposits. Those backing this side believe the funds are "stickier" than originally thought. They believe that depositors have had plenty of opportunity to seek out better returns (i.e. stock markets, real estate, etc.). The truth is likely somewhere in the middle.

But with the prospect of higher short-term rates, the industry may get its first look at which argument is more accurate.

Despite your bias regarding the "surge" deposit debate, 2017 could be the first time in years that deposit costs start to inch up.

So, have you identified your potential exposure? What is your "game plan" if the FOMC increases rates, as anticipated? How much liquidity will your organization need if additional loan growth is necessary? How competitive is your deposit market and how will you react to specials designed to "steal" your market share?

Most organizations have already "dug" into their deposit base in an effort to decrypt which relationships may be in jeopardy. That analysis gives management an informed estimate of the potential level of exposure which resides on the balance sheet.

In some cases, this warrants discussion of the introduction of new "shelf" products to recapture those dollars, but in others it simply means the organization will utilize the wholesale markets to backfill.

It is also important to comprehend how the remainder of the balance sheet behaves after an FOMC rate increase, without altering deposit pricing.

For asset-sensitive organizations, an FOMC increase adds additional net interest income. On the other hand, the converse may be true for liability-sensitive organizations.

Understanding this computation gives the forecaster better insight into the impact of higher rates on the net interest expense levels of the bank.

With the specter of higher rates, focus on deposit strategy has sharpened. In order to forecast appropriately, it's important to understand your deposit base and how it may be influenced by the FOMC during 2017.

4. Credit Expectations

By most metrics, credit performance has been very strong across the industry. Net charge-offs to total loans is down to 11 basis points (per Q2 FDIC statistics) from 87 basis points just five years ago.

And while Janet Yellen was quoted as saying that economic recoveries don't end due to "old age," many would acknowledge that the relatively benign credit environment could begin to change.

Consider the confluence of double-digit appreciation to residential real estate values, declining cap rates on CRE, low unemployment, historically low interest rates along with other factors conspiring to the healthy state of the credit environment.

As a result, many organizations have performed some form of credit stress testing. The spirit of the exercise is to quantify the impact of unforeseen credit loss and the related impact on the capital profile of the organization.

While the probability of a return to the default levels from the recent recession seems remote, it is critically important that your bank understands its exposure to changes in credit dynamics.

Further, given the strategy to "outrace" margin compression with additional loan growth, will the capital position accommodate these aspirations if credit starts to deteriorate? Accordingly, will growth assumptions need to be tempered? These are key considerations which may influence the overall strategy.

Be realistic and plan accordingly

"The wind and the waves are always on the side of the ablest navigator."—Edmund Gibbon

Make no mistake, 2017 will present a challenging environment for all banks. Weather conditions may stiffen, but proper planning will position your institution for success. Before you pull out your chart and plot your course, give long and thoughtful consideration to the key issues presented above.

I'd rather be the realist who successfully navigated through rough waters than the optimist who blames it on bad weather or the pessimist who is still at the dock waiting for better weather.

So where are you taking your ship in 2017?

About the author

Vincent Clevenger is a managing director at Darling Consulting Group. In this position, he currently advises financial institutions on balance sheet management strategies. He takes a practical approach to the demands that the economic and regulatory environment place on his clients. Since joining the firm in 2003, he has worked in a number of capacities within DCG assisting clients in all aspects of ALM including process reviews, model validations, policy reviews, capital management, and contingency liquidity planning. He also serves as the product manager for DCG’s capital planning and stress testing products.

Tagged under Bank Performance; Mergers Acquisitions; Big Data; Risk Management; Rate Risk; Feature; Feature3;