Get deposit ducks in a row now

And don’t pay 85% of customers for rate 15% want

- |

- Written by ALCO Beat

ALCO Beat articles featured exclusively on bankingexchange.com are written by the asset-liability management experts at Darling Consulting Group.

ALCO Beat articles featured exclusively on bankingexchange.com are written by the asset-liability management experts at Darling Consulting Group.

By Keith Reagan, managing director, Darling Consulting Group

Regardless of any given positive economic indicator reported, it seems one can always find an offsetting indicator pointed in the complete opposite direction.

The unemployment rate has been improving, yet there has been minimal wage growth (much less wage pressure). The Fed reiterated there is substantial slack in the employment picture in its most recent testimony.

Asset purchases by the Federal Reserve are winding down, while China is buying more than ever before.

Positive growth in the U.S. (this quarter that is) is countered by trouble in Europe.

The ECB and China have recently lowered rates, while the overall consensus here seems to be that the Fed will change course and begin to tighten monetary policy in the middle of 2015.

Thus, we come to a critical point: ALCO strategies should never be employed assuming a specific rate forecast.

How would that have worked out over the last five years when many people “knew” rates were going to rise?

Answer honestly!

However, you must commit to something to move forward, and so the remainder of this article will assume the market consensus is correct and that short-term rates will be increasing in 2015. As such, banks are only three to four quarters away from feeling pressure on their funding costs. I have already seen—and honestly suggested to some clients—deposit specials in the 1.00-1.25% range on both non-maturity and short time deposits.

Getting your ducks in order

However, before raising the rates on your existing accounts and/or introducing a new special, much work needs to be done internally.

How much of your deposit base is truly rate sensitive? Answering this question can be done by gut, by core deposit study, and anything in between. But the question must be answered.

What other questions should you ask?

• For your liquidity and interest rate risk models, how often are the assumptions updated and when was the last time they were validated by a study?

• How much growth have you seen in deposits in the last five years?

• Is the growth abnormal (i.e. surge)?

• Has there been a shift from CDs to non-maturity deposits?

• Have average balances increased? If so, in which accounts? Are they retail or business?

• Have you increased the number of deposit accounts?

• Have you stress tested your liquidity and interest rate risk models?

• Can you afford to lose deposits, in terms of liquidity, interest rate risk, and earnings?

Conducting marginal cost of funds analysis

Once the rate-sensitive customers are identified, a multitude of deposit pricing strategies can be employed. One very simple tool we at DCG have used through many different rate cycles to help identify the best strategy is the marginal cost of funds analysis.

This analysis can be used to analyze the risk reward of deposit pricing increases (or decreases) as well as to determine the break-even point at which it either does or does not make sense to change deposit rates.

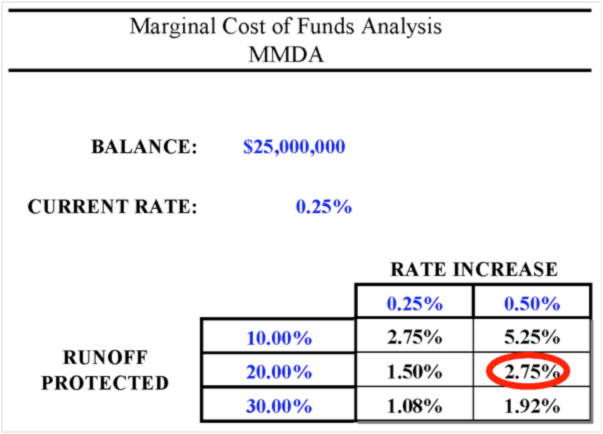

In the simple example of Exhibit 1, a bank is considering increasing its money market account rate 50 basis points to satisfy the contingent of “squeaky wheel” customers.

Suppose that this segment of customers makes up 20% of the deposit base (which in this example is $5 million). Using the marginal cost of funds analysis, the breakeven rate at which the bank could replace the $5 million is 2.75%, assuming the money leaves without an increase in the existing rate.

In other words, the bank could replace $5 million with other funds costing as much as 2.75% (through borrowings or other sources) without increasing current interest expense. That is because it will have maintained the rate on the 80% of money market accounts that is not primarily concerned with rate.

If a bank increases the overall portfolio 50 basis points to satisfy a small contingent of depositors, it is in essence paying that group 2.75% because it is giving the other 80% a “raise” it was not looking for.

Simply doing the math, $20 million at a rate of 0.25% and $5 million at a rate of 2.75% creates the same interest expense as $25 million at a rate of 0.75%.

Another strategy may be to introduce a new premium deposit product to attract new dollars and to identify existing customers who are rate-sensitive. This strategy would allow you to offer a competitive product, and only pay those looking for a higher rate.

How do you support this move?

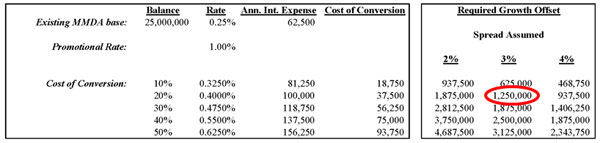

Either way, interest expense will increase. How will your bank pay for that increase? One way will likely be to grow your balance sheet. Again, a simple marginal cost of funds break-even analysis, as shown in Exhibit 2, can help determine how much growth will be necessary to offset the increase in interest expense.

For a larger version, click on the image.

For a larger version, click on the image.

In this example, a promotional product is introduced and 20% of the existing accounts shift to the new product. To cover the additional interest expense associated with the shift, the balance sheet would need to grow $1.25 million at a spread of 3.00% to cover the additional cost of the shift.

Now is the time to strategize

These simple analyses can and should be used as part of your strategic planning process to help determine if a particular deposit strategy makes financial sense.

Assuming we are three to four quarters from a rising rate environment, your competitors are having conversations about deposit growth/pricing strategies.

Some of you should use these and other tools to help play defense against your competitors’ deposit pricing strategy while others should perform analysis to help you play offense and steal your competitors’ deposits. Either way, you should be formulating strategies today to ensure the best possible outcome for your balance sheet.

About the author

Keith Reagan is a managing director at Darling Consulting Group. He has 20 years of experience working directly with community banks, helping them improve their overall performance through proactive management of liquidity, interest rate risk, and capital. He works to develop strategies that best fit the risk/return dynamics of their balance sheets. Reagan has served on the faculty of ABA's Stonier School of Banking, has written many articles for a variety of professional publications, and is the editor of DCG's monthly periodical, the DCG Bulletin.