A quiz about rising rates

Is your bank really ready? Really?

- |

- Written by ALCO Beat

ALCO Beat articles featured exclusively on bankingexchange.com are written by the asset-liability management experts at Darling Consulting Group.

ALCO Beat articles featured exclusively on bankingexchange.com are written by the asset-liability management experts at Darling Consulting Group.

By Keith Reagan, Darling Consulting Group

Since rates hit near 0% in December 2008 there has been concern about being prepared for when rates will rise again.

Since then, many banks have employed strategies to reduce exposure to rising rates—yet rates have not risen.

If your bank is one of the banks that took strategic action, I assume you are happy despite the fact you bought insurance you have not collected on yet. I say this because I assume your bank was liability sensitive, and truly needed to buy protection against rising rates.

Perhaps, however, you bought protection (i.e. funding extension, caps, etc.) not because you needed it, but because “it would look good someday.” Then you are likely unhappy with that decision.

Maybe, in your own mind, you called it a “bet.”

That type of decision is the opposite of what asset/liability management should be. Strategic action to protect your bank should be a hedge—not a bet.

Multiple choice—which fits?

So let’s start with your interest-rate-risk profile by taking the following quiz.

Is your bank exposed to:

a. Rising rates?

b. Falling rates?

c. The current rate environment?

d. All of the above?

If you answered A, how exposed to rising rates is the bank? Are you approaching your bank’s policy guidelines?

Is the exposure immediate or is there a delay? How high do rates have to go before exposure exists? What is the probability of that scenario in the foreseeable future?

If you answered D, is the exposure to the current rate environment or to a falling rate environment worse than exposure to rising rates?

If it is, should you be buying protection against rising rates that will worsen the exposure to current or falling rates?

In all likelihood, if you answered D, you probably cannot afford to give up current earnings and buy protection against rising rates.

If your bank does not have exposure to rising rates, have you stress tested the major assumptions embedded in your asset-liability model?

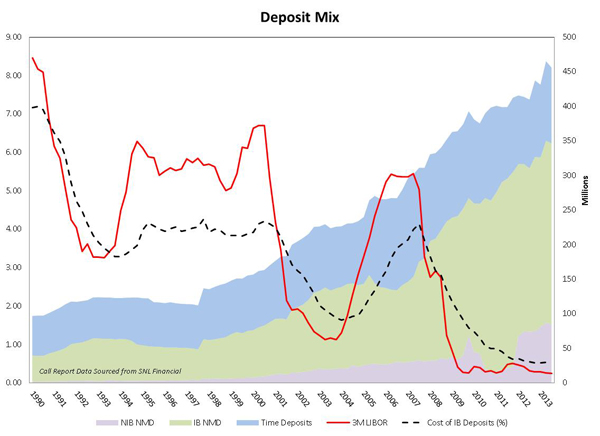

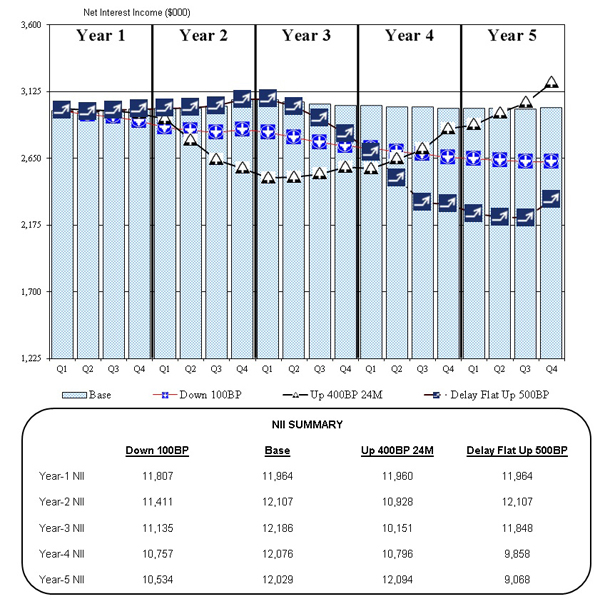

1. Potential deposit volatility or “surge.” Has the bank experienced abnormal deposit growth since 2008? See the graph below depicting the surge in the deposit mix.

For a larger version, click on the image.

For a larger version, click on the image.

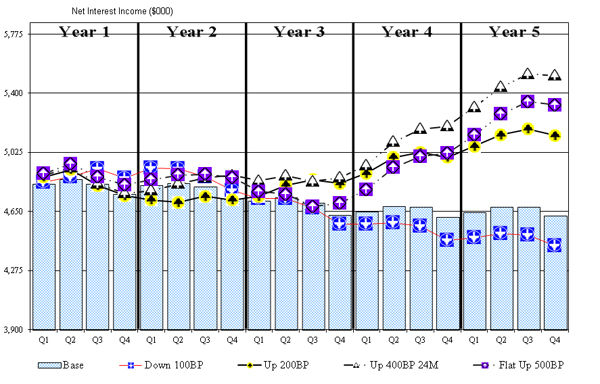

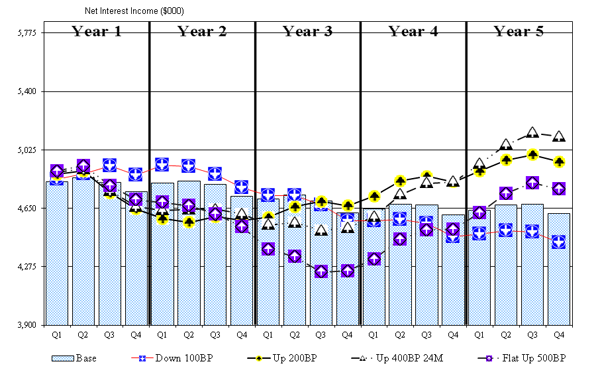

2. Deposit pricing betas. Go back to the last rising-rate environment and compare rate movements and ending rates with what you are currently assuming in your asset-liability model.

How reasonable are the assumptions compared to the past and in conjunction with expected deposit strategy going forward?

Have you conducted a deposit study (internally or externally) as support for potential volatility and beta assumptions? Quantitative and qualitative analysis should be used.

The following simulation graphs are from the same bank. The upper graph uses core deposit study results (quantitative) on volatility and beta. The lower graph uses management’s qualitative analysis. (Editor’s note: The larger version obtained by clicking through is side by side, with the upper graph on the left and the lower one on the right, of the larger version.)

Which is correct?

For a larger version, click on the image.

For a larger version, click on the image.

3. Loan pricing spreads. How high do the rates on new cashflows increase in your model? If current production 5-year commerical real estate is at 4.00%, does that rate increase to 8.00% in a +400 basis points scenario? Is that reasonable? Or will spreads contract (and/or the yield curve change shape) in a rising rate environment?

Acting on your answers

After performing stress tests on all major assumption groups, retake the quiz above.

Are you exposed to rising rates now?

If not, you do not need to buy insurance for rising rates.

But if you are exposed, what should you do?

First, realize (and explain to board and shareholders) that there is a cost to insurance.

Whether or not you write a check today, strategic action to reduce exposure is buying insurance, and there is a cost. There are many different strategies that can be employed to reduce potential exposure to rising rates (some more immediate and some longer-term), but they can be reduced to two main strategies: shorten assets or lengthen liabilities.

The shorten assets strategy

As long as the yield curve is positively sloped, this reduces earnings.

• Shorten investment and loan strategy. This can be done over time (as investments and loans cashflow) or immediately through the sale of existing assets.

• Replace investment cashflows with floating-rate assets.

• Generate more floating-rate loans in your marketplace.

• Purchase floating-rate loans from other banks.

• Use interest rate swaps to artificially shorten assets.

• Purchase interest rate caps.

Above and beyond the earnings impact, there is risk associated with each of the above strategies.

Investments may be at a loss that could be too much to accept, or classified as held to maturity.

Generating more floating-rate loans in your marketplace is much easier said than done.

You may need to add loan types that you currently do not offer.

You may have to acquire talent to generate these loans (i.e. C&I expertise).

And most of your customers likely want a fixed rate, not a floating rate.

Loan purchases can be difficult—you must be comfortable with another bank’s credit assessment—especially if you have not done them before. Derivatives offer an additional set of accounting and education challenges for your management, board, customer, and regulator.

The lengthening liabilities strategy

This can be done either in the retail or wholesale markets.

• Longer-term retail CDs.

• Extend wholesale funds. Can be done with longer-term Federal Home Loan Banbk advances or brokered CDs, or artificially with derivatives. There is no one-size-fits-all. Use the appropriate funding source depending on your overall liquidity and interest rate risk position.

• Grow core deposits. This is a longer-term strategy, but may be the best defense against rising rates.

• Acquire deposits.

Similar to shortening assets, each of the liability lengthening strategies has potential challenges.

Most of your retail CD customers want to stay within a 12-18 month window unless you overpay them and include options like penalty-free withdrawals. (But ask yourself: With these accomodations, is the CD truly extended?)

Deposit growth either organically or through acquisition can be expensive or may take too long, depending on the amount of your potential exposure to rising rates.

Any of the above strategies should be thoroughly vetted and modeled as part of ALCO. Be sure to focus on not only the reduced exposure to rising rates but also the cost associated with the strategy.

How do the current and falling rate scenarios look after employing the strategy? This is a critical part of the risk/return analysis and will help you determine if purchasing insurance for rising rates should be done.

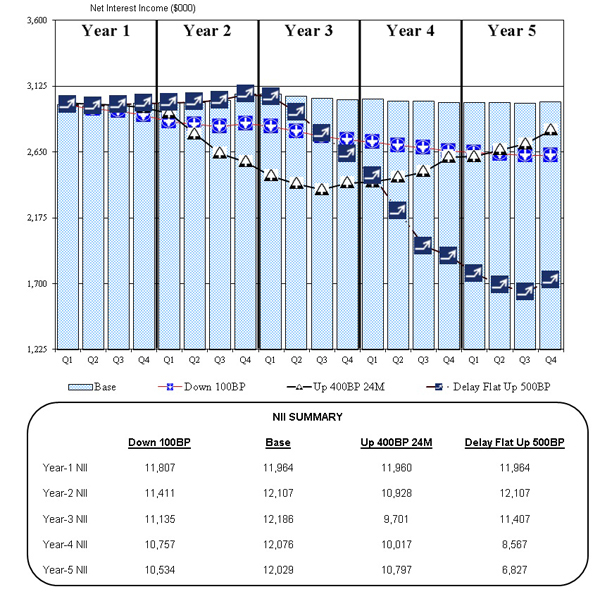

Consider the “earn to grow” strategy

One often overlooked strategy to prepare for rising rates: Earn as much as you can today—without compromising your risk tolerance—so that you can build capital to grow your way out of potential exposure when rates rise.

Think of this: Every dollar that you earn today is another $8-$10 you can lend when rates do rise.

Of course, this assumes that rising rates are due to increased economic activity and an increased ability to grow loan portfolios. The simulation below includes a normal run rate of loan growth in the rising rate environment (lower graph).

While there is still exposure, it is different enough from the static position that it impacts strategic direction.

For a larger version, click on the image.

For a larger version, click on the image.

What you do should fit your circumstances

There are banks that should employ the more immediate strategies listed above.

And there are banks that should employ the longer-term strategies, because they have less sensitivity and/or more time.

And there are banks that should be doing the opposite of the listed strategies—they should be lengthening assets and shortening liabilities because they are asset sensitive. An asset-sensitive bank should not be worried about rising rates.

Ultimately, potential strategic action should come back to your answers on the quiz.

You need to know your position—admittedly easier said than done with the amount of work required to have a proper interest rate risk assessment today.

And then you must ask yourself one last question: Can I afford not to reduce my exposure?

If the answer is no, you need to take strategic action!

This goes for banks that answered A,B, C, or D.

About the author

Keith Reagan is a managing director at Darling Consulting Group. He has nearly 20 years of experience working directly with community banks, helping them improve their overall performance through proactive management of liquidity, interest rate risk, and capital. He works to develop strategies that best fit the risk/return dynamics of their balance sheets. Keith has served on the faculty of ABA's Stonier School of Banking, has written many articles for a variety of professional publications, and is the editor of DCG's monthly periodical, the DCG Bulletin.