Effective Loan Pricing – Why It’s Imperative Now More than Ever

Today’s environment is especially challenging

- |

- Written by Darryl Mataya, Abrigo

It is probably not news to you that financial institutions are in a unique and challenging rate environment. As writers and advisors we often overstate the difficulty and challenges of any current environment. For example, no matter what anybody said about rates and the economy in 2015, it was still incredibly cheap to borrow money, whether from depositors or from wholesale markets. But today’s environment is especially challenging.

Even before the Fed rate cut in July, mortgage rates were starting to drop and now have fallen to their lowest levels in three years. Prime- and LIBOR-based loans are earning about 50 basis points less than earlier this year, and those yields are certain to drop again if the Fed cuts rates again this fall. But borrowing, in the form of cost of funds, hasn’t really gotten any cheaper yet.

And unlike 2012, if loan demand increases due to lower rates for consumers, deposit costs are not likely to decrease as much because liquidity, or available excess deposit funding, has mostly dried up over the past five years. This demand for retail deposits is keeping deposit rates higher than they typically stay when wholesale rates start to drop. In short, a nasty squeeze is being applied to your net interest margin.

Is the stage set for inevitable lower yields?

One of the things that makes this difficult is that asset/liability models probably didn’t predict this. When we forecast the future in these models, standard practice is to assume that rate movements occur in parallel. If we model a 200 basis point rise in rates, our models assume all rates rise by the same absolute values. In practice, this never happens.

For example, the yield curve went from positively sloped in the fall of 2012 to a convex-shaped curve in 2019 where today, the cost of overnight funding is higher than borrowing for 2-3 years. In retail deposit markets this shows up in the form of short-term CD rates being almost as high as long-term CD rates. In asset/liability speak, institutions that thought they were asset sensitive in a rising-rate environment were not, because their short-term funding costs rose more than predicted by models. And now that rates are dropping, the yield on loans at some institutions could drop more than their cost of funding.

But are these lower yields inevitable? Let’s compare institutions, because the story can be different.

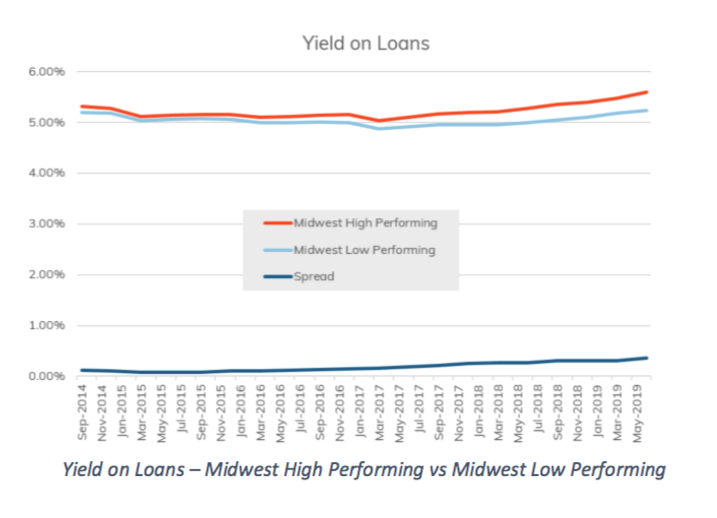

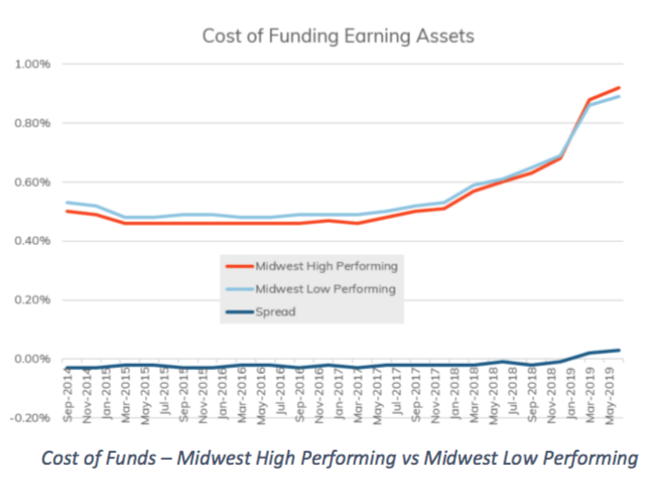

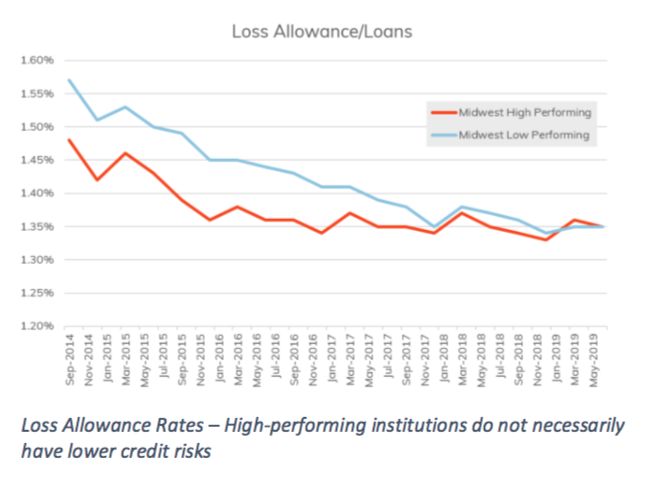

The following charts show the relative performance of 248 institutions in the Midwest that we consider high performing and 980 Midwest institutions that we consider low performing. (In these peer groups, the high-performing banks were those with ROE over 16% and asset size less than $1.5 billion. The low-performing banks were those with ROE less than 9% and asset size less than $1.5 billion.) In examining the loan growth, cost of funding, and performance of these institutions over the last five years, we have noticed some interesting differences between these two groups.

For example, we often discover that high loan growth rates do not always translate into more income. We also have noticed that there isn’t a large difference in funding costs between the two groups. And in fact, the funding costs of our high-performing Midwest banks had been running higher than the lower-performing ones for the past year. While there are varying reasons why some institutions perform better than peers, we typically see better yields on loans at high-performing institutions, and we have noticed that difference with several peer groups.

Factors behind lower yields on loans

There are a couple of fundamental reasons why one institution will earn less yield than another. The first is loan mix. If you are heavily concentrated in retail mortgage loans you keep in your portfolio and you price aggressively, you have a tough time making money because of the commodity nature of these loans. On the other hand, if you mostly do specialty commercial lending and have a particular expertise, it is likely you are earning more yield.

A second possible reason: Some institutions price aggressively with the same products their competitors offer in order to promote growth. So, as price leaders, they are willing to accept less yield for the same loans in order to build volume.

But there is a third possible reason some institutions earn less yield on loans, and this reason is often less obvious. It may be that you are earning less on loans because you aren’t being paid enough for the risks you are taking on. Lenders earn a spread on loans because they have to cover their operating costs, but also because they take on credit risk, interest rate risk, and liquidity risk. You know that lending to people with lower credit ratings means you need to charge more to cover the potential additional credit losses.

But how much more do you charge? In the majority of institutions we talk to, the lending function looks to market and competitor rates to make these decisions. And with commodity loans like a conventional 30-year mortgage, institutions have to price what the market will bear. Are these market-based rates enough to cover costs, especially when compared to other retail loan alternatives available?

Options when NIMs are squeezed

So, what do financial institutions do about this squeeze they are in today? Do they focus on lowering operating costs? Some institutions are certainly considering that, as we’ve already seen one case of a large regional bank announcing layoffs and blaming them on the net interest margin scenario described above. Other institutions might look at continued growth as a solution. “If I can take market share away from other institutions, I mitigate the net margin loss with higher volume,” is the way the thinking goes. There is another choice. Your most valuable asset/liability management tool is your retail pricing. You make the majority of your income from net interest margin; therefore, pricing successfully is your best opportunity to maintain that margin.

What is the best way to price successfully and become a high-earning institution? We think an essential component for long-term success is to use a disciplined loan pricing process that employs some kind of pricing model to quantify the various risks you are taking on. We firmly believe that high-earning institutions find ways to get paid more for the risks they take on. For example, it is common for institutions to avoid longer-term fixed rate loans because of the concerns about the interest rate risk they are taking on.

But financial institutions have been making fixed rate loans for a long time. We have the data and the techniques to evaluate how much that risk costs to hedge. And we know how valuable a fixed rate feature is to a borrower, because they express their preferences for that option via the market. Your job is to evaluate that value and decide if you want to price enough to satisfy the cost of the risk.

Effective loan pricing starts with a framework

An effective loan pricing process starts with a decision framework that evaluates all of your opportunities and makes decisions based on institution-level objectives. For example, some institutions will price in order to earn a specific loan ROE or ROA, where others will price just enough to earn more than alternative wholesale investments. Once that framework is in place, a model is necessary to evaluate and compare different loan types and credit grades.

In order to capture all risks and costs, loan models need to capture all of the specific cash flows, which include regular amortizing payments, prepayments, operating expenses, and a credit-loss projection. After that, a model must account for interest rate risk and option risk. This is usually accomplished using funds transfer pricing techniques to calculate the hedge necessary in order to eliminate interest rate and option risk. Finally, a competent loan model can also assess the relative value of relationship bundles – calculating the value of bringing in deposit accounts with loans, or the potential to discount loans when multiple loan types are originated with a single borrower.

With a pricing mechanism in place, a regular practice can be established to make pricing decisions. With commodity or rate sheet loans, a pricing committee will periodically review performance (origination volume) and relative profitability compared to goals and decide when and where to make changes to product configuration and pricing.

With commercial loans, a model can be used to evaluate individual loans or loan and deposit relationships to ensure that institution objectives are met while meeting borrower needs where possible. For example, one of the best uses of a model in bidding on commercial deals is learning and knowing when to walk away from unprofitable relationships.

Lower interest margins aren’t inevitable

We believe that lower interest margins are not inevitable. If you have loans indexed to Prime or LIBOR, then you clearly are going to lose yield on those loans as those market rates fall. But you have ALCO and pricing tools available to mitigate those losses as market rates change. Fixed rate loans are not obligated to follow the market; many institutions just assume they have to in order to maintain their balances of originations.

But without a disciplined process using pricing tools, you allow the market to define rates and therefore your spread. You have other choices. In order to create a high yield loan portfolio, you have to understand where and why you earn yield, and whether you are being compensated for the risks and costs associated with those opportunities.

Tagged under Risk Management; Risk Adjusted; Rate Risk; Credit Risk; Operational Risk; Feature3; Feature;