The bear is waking up

Should your bank kick it awake? Or hope it naps again?

- |

- Written by ALCO Beat

ALCO Beat articles featured exclusively on bankingexchange.com are written by the asset-liability management experts at Darling Consulting Group.

ALCO Beat articles featured exclusively on bankingexchange.com are written by the asset-liability management experts at Darling Consulting Group.

By Keith Reagan, managing director, Darling Consulting Group

The annual cycle of black bear activity and hibernation has five stages:

1. Hibernation

2. Walking Hibernation

3. Normal Activity

4. Hyperphagia (gorging to add body mass)

5. Fall Transition

Hibernation means continuous dormancy for up to seven and a half months. Walking hibernation is the two-three weeks following the emergence of hibernation (waking up, but still not at normal activity levels). Then there is a period of normal activity, followed by stage 4 and 5 as the bear transitions back to hibernation.

The sleeping bear that is your deposit base has been hibernating for the better part of the last decade.

It feels like we are currently in the walking hibernation stage (at least) in most deposit markets. Your customers are emerging from a decade of rates near 0% and are beginning to act as they have in the past.

If your market is not nearing the normal activity stage yet, consider yourself lucky. You will be there soon!

No matter the stage of the cycle your customers are in, there are strategies that can be employed to grow deposits; manage funding costs; and expand customer relationships while managing liquidity and interest rate risk. The keys to any successful strategy are pre-planning, execution, and debriefing.

Pre-planning

How well do you understand your deposit base?

Not all depositors have the same needs as one another. What are the key differences within the deposit base that you currently monitor?

The size of the deposit is one part of what may cause differences. Others include demographics, length of relationship, number of relationships with the bank, customer profitability, etc.

As normal activity returns (i.e. customers looking for higher rates), do you have a good handle on the specific attributes that are important to the different segments of the deposit base?

Are you going to increase deposit rates across the board, only on certain tiers, or selectively for certain customers?

What have you done already, and what have you learned from it?

Depending on liquidity, interest rate risk and earnings profiles, some institutions need to be proactive, while others should be more reactive. Which approach is right for your balance sheet?

Execution

The execution of your strategy will be dependent in part by the folks on the front line, many of whom were not in their current roles during the last rising rate cycle. Training on the specific strategy you are trying to employ is critical, as is training on objection handling (meaning: how to handle the customers who are unhappy with your strategy).

Debriefing

Many of you have already implemented certain initial strategies. How well did they work and what did you learn from them? The debriefing is critical to the success of the next strategy!

Current economic environment

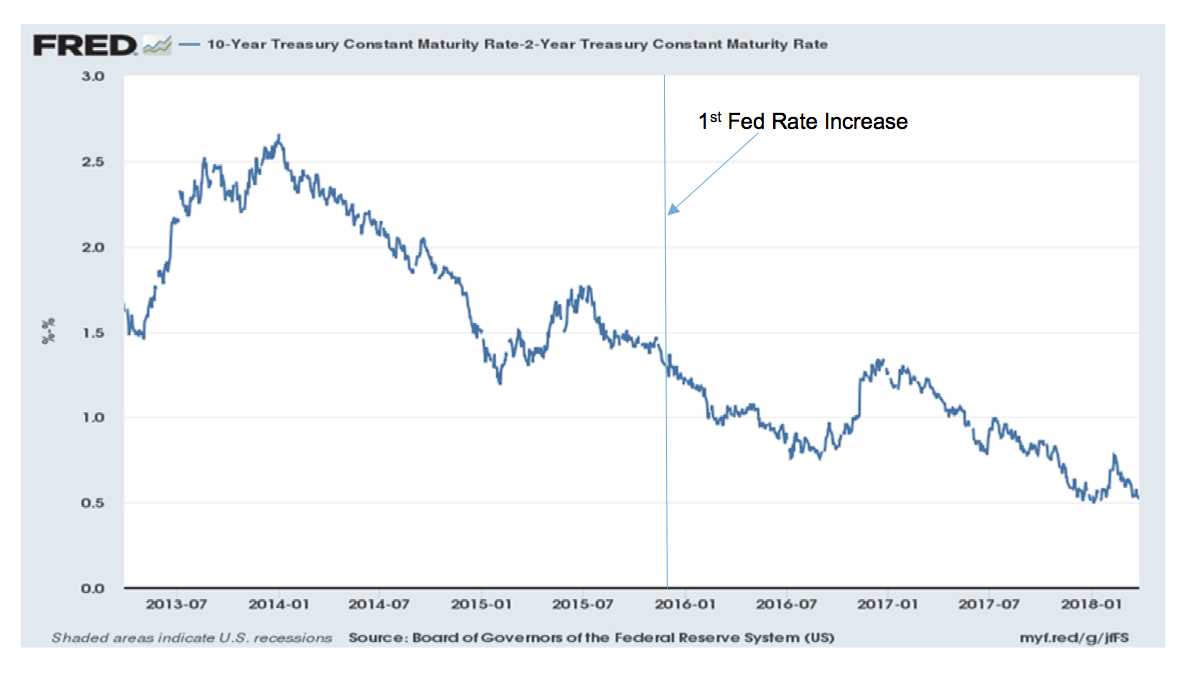

The yield curve has lost substantial spread since the Federal Reserve began increasing short-term rates. The following graph highlights the relationship between the 2 and the 10 year Treasury bond rates. The pressure a flat yield curve causes increases the importance and priority of strategic action today.

The awakening bear does not care that the yield curve is flat and that margin is coming under pressure. The bear is hungry and looking for something to eat.

Should you feed the bear?

For some readers the answer is “yes,” while for others the answer is “no” (and some fall in between). It depends on the current balance sheet as well as near-term and long-term goals.

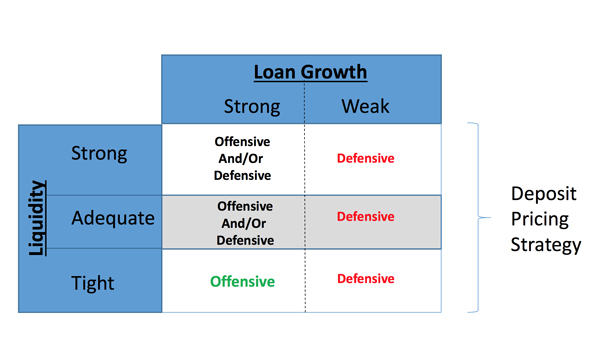

What is your bank’s current liquidity position?

The Fed is in tightening mode; investment cash flow has shifted to loan portfolios; and wholesale funds have been supplementing balance sheet growth. As such, industry-wide liquidity levels are on the decline. What about your balance sheet?

The current liquidity position should be a linchpin for strategic discussion at every ALCO meeting. How much liquidity do you have? What is the forecasted loan growth and how much liquidity is needed? If funding is needed, what type of funding is desired (i.e. retail or wholesale)?

Those banks with strong liquidity positions can likely have more intestinal fortitude to hold and lag deposit rates and be defensive in their approach. On the other hand, while those with tighter liquidity likely need to be more proactive and have an offensive strategy.

Where does your institution fall in the following chart?

If loan growth is strong and liquidity is tight, obviously aggressive offensive strategies are necessary. However, if loan growth is not robust and liquidity is strong, a defensive posture on deposit pricing would be recommended.

For most banks, it probably isn’t that cut and dried. Elements of offense and defense are needed.

An aggressively priced deposit product for new money only is an example of an offensive and defensive strategy combined. Banks that have employed this type of strategy are doing so to grow new deposits without pricing up the existing base (meaning: grow without waking the sleeping bear). Similar strategies have been executed flawlessly by some, while it has not worked for others.

There is no one size fits all deposit strategy. Each market and deposit base is unique. One commonality will likely be that deposit customers will be looking for higher rates in the next 12 months than they did in the previous 12 months. How do you keep them happy without overpaying?

Answer some key questions

Before raising the rates on existing accounts and/or introducing a new special, pre-planning needs to be done.

First, how much of your deposit base is truly rate sensitive? Answering this question can be done by gut, by core deposit study, and anything in between. But the question needs to be answered.

Other questions to ask:

• Have you calculated the potential volatility and current attrition levels within the deposit base?

• Are you starting to see a mix change from low rate accounts into specials (either shifting on your balance sheet or to your competitors)?

• Can you identify accounts that are declining? These accounts may be at risk.

Once the rate sensitive customers are identified, a multitude of deposit pricing strategies can be employed. Strategies include:

• Marginal Cost of Funds Approach (analysis showing the mathematical indifference point between raising rates “across the board” versus selectively increasing segments of the deposit base)

• Creating a new product

• Changing tiers within existing products

• Increasing rates across the board

Liquidity is only one piece of the puzzle. The interest rate risk profile of the balance sheet needs to be factored into the equation as well. Is the balance sheet well matched, asset sensitive, liability sensitive, or a combination of all three?

Asset Sensitive

Strategically much can be done to improve the profile even if a rising rate environment is beneficial to the bottom line. Deposit pricing strategies (as described above), as well as investment and loan extension strategies, can likely improve earnings and reduce potential exposure to falling rates. (Remember, the bear will hibernate again someday). Improved earnings will help offset the likely increased funding costs that are associated with the awakening bear.

Liability Sensitive

Understanding your deposit base will not only help improve liquidity but also reduce potential exposure to rising rates. Lagging rates, offering new products, and adding wholesale funds will help.

More can be done. Does projected growth impact your profile positively or negatively? Can you afford insurance against rising rates if other strategic action (i.e. funding extension) is needed? As with any insurance, this can be costly. If these types of strategies are necessary for your balance sheet, the importance of the cost savings strategies above take on even more importance.

Looking ahead

All banks are going to experience a certain amount of deposit outflow, attrition, and rate increase in 2018. Some banks are hoping their deposit customers will continue to hibernate. Meanwhile, others are not only poking the bear, they are kicking it with rates at 2% and above.

Understanding your balance sheet profile and employing different strategic action will turn the cost of feeding the bear into potential benefits for your institution.

About the author

Keith Reagan is a managing director at Darling Consulting Group. He has more than 20 years of experience working directly with community banks, helping them improve their overall performance through proactive management of liquidity, interest rate risk, and capital. He works to develop strategies that best fit the risk/return dynamics of their balance sheets. Reagan has served on the faculty of ABA's Stonier School of Banking, has written many articles for a variety of professional publications, and is the editor of DCG's monthly periodical, the DCG Bulletin.

Tagged under Big Data; Feature; Feature3; Mergers Acquisitions; Financial Trends; CSuite;

Related items

- Global Instability and Rising Treasury Yields, but Markets Open Higher

- “Stablecoin Strategy” Is a 2026 Question for Banks, Not a 2027 One

- Banks Need to Reconsider their Role in an AI-Driven Future

- Tokenization Could Reshape Financial Markets, Says IMF

- UBS Expands US Banking Push for Affluent Wealth Clients