Disruption: How must your bank change?

How 4 tech trends—and changing attitudes—will transform banks and bank regulation

- |

- Written by Jo Ann Barefoot

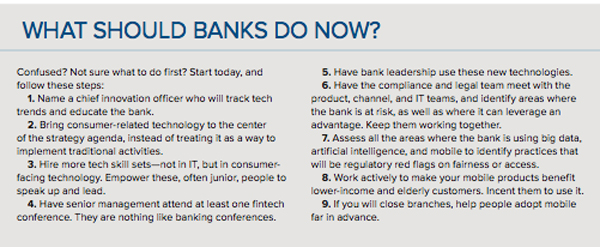

Banks—and their regulators—must get big data, artificial intelligence, mobility, and voice technology right, according to banking expert Jo Ann Barefoot in this special viewpoint article. The main article is followed by a special strategy section, “What should banks do now?”

Banks—and their regulators—must get big data, artificial intelligence, mobility, and voice technology right, according to banking expert Jo Ann Barefoot in this special viewpoint article. The main article is followed by a special strategy section, “What should banks do now?”

There’s a phone app called MeetCARROT that helps people do things we tend to shirk. I’ve listened to the app repeatedly, and I still laugh out loud every time.

MeetCARROT’s alarm clock tool, speaking in a stern robotic voice, says things like, “Wake up, lazy human!” The app’s exercise coach calls itself, “Your Judgmental Fitness Overlord,” and promises a “7 Minutes in Hell” workout.

Welcome to the future of banking.

Forget marble columns and pin-striped suits. People are banking in new ways as technology brings changes that reach far beyond products, channels, and customer habits. Technology is changing how people interact with money.

Not everyone will go, or wants to go, high tech, of course. And the market won’t transform overnight. Still, these shifts are gathering speed and power.

Will they be good? Or will they be bad?

They will be both—for consumers and for the industry.

Shifting landscape

That is the nature of innovation. It always brings help and harm—mixed together.

Innovation also tends to be underestimated, even while simultaneously being overhyped. Bankers today generally underestimate the pace and vastness of the disruption they face. One reason is that the changes are so novel—intrinsically hard to grasp. Another reason: Most of the coming change is happening outside the typical banker’s field of vision. Also, compellingly, banks—and regulators—have been kind of busy lately.

Recently, Alan Lane, CEO of Silvergate Bank, in La Jolla, Calif., pointed out to me that not one, but two defining events debuted in 2007.

One was the financial crisis. The other was Apple’s introduction of the iPhone. In the intervening years, bankers and policymakers have been consumed with disposal, survival, cleanup, and recovery, while the iPhone and many other business-changing developments have been evolving in plain sight—with arguably even bigger ultimate impacts for banking institutions and their customers.

Recipe for confusion

It has become commonplace to observe that financial services faces tech-driven disruption of the kind that has remade industries from publishing to taxis.

What has not yet been widely recognized is that this disruption is unlike any other. Consumer financial services is the first industry to face disruption while also being vital to everyone and extremely highly regulated—with probably the most complex regulatory structure of any sector. Five federal agencies directly supervise financial institutions and about 25 regulate some aspect of financial products and practices. There also is the regulatory infrastructure of 50 states and, for some banks, international law.

The intertwining of banks and regulation means that technology—and the changes in attitude and appetite that accompany its adoption—will disrupt the industry and the regulatory system.

In spite of their talents and dedication, regulators and policymakers will find it impossible to avoid big problems as huge waves of change hit a system that is fragmented; designed to be deliberative; and was built to address 20th century issues with 20th century tools.

Agencies will struggle to be consistent, internally and with each other, causing industry confusion. Their rules will have shrinking shelf life as product innovations morph out from under them. Their rulemaking processes typically take years; technologies and markets change daily.

This will force regulators to rely more on principles-based rather than rules-based supervision, but the principles will lack clarity as they rapidly evolve. This will bring rising subjectivity and leave banks unsure of how to comply.

There also will be jurisdiction problems. If phone companies offer loans, will the Federal Communications Commission be a financial services regulator?

What will happen as new players insert themselves between banks and customers through apps or by offering services through, say, social media? How will regulators maintain the integrity of the bank charter and system? Who will be responsible for disclosures? Can regulators find and reach small startups creating apps? How will privacy, data security, and fair treatment be protected?

Will banks be held to higher standards and forced to retain high cost structures? If so, will the industry lose market share due to unique regulatory burden?

Disruption of the regulatory system will, in turn, force a third disruption: the industry’s compliance systems.

Bank compliance grew up over decades to be highly effective at rule following. But lying ahead now are years of upheaval in which clear rules will lag far behind changing subjective regulatory “standards.” Throughout this transition, rising consumer harm will fuel aggressive enforcement based on regulatory discretion. Banks will need new compliance strategies, structures, and skills.

There is an almost universal assumption that regulation and innovation live in different worlds, needing efforts by different people with different mandates and skills. I would argue that the only way to avoid doing both wrong is to integrate them. This matters because bank executives tell me that technology and regulation rank as their top challenges. They know that if they get either one wrong, their bank will be hamstrung. What most have not yet realized: If they get either one wrong, they will inevitably get both wrong. The industry needs to change how it does both.

Four trends changing all

A half-century ago, Ralph Nader published his book Unsafe at Any Speed. It launched the movement that aims to protect consumers through regulation. In banking, the regulatory focus stressed mandatory disclosure.

While the effort has done some good, we can’t say it was a success. Policymakers built a massive edifice of financial consumer protection rules, and the industry, a colossal compliance machine. Years were spent fostering financial literacy. Yet we are still cleaning up the aftermath of the mortgage crisis, and millions of people are routinely harmed by money choices they don’t understand. Millions cannot access mainstream services.

These problems have been apparent for years. Instead of a vigorous debate over what the goal should have been, things calcified into arguments over quantity—less regulation or more regulation.

Technology is breaking that impasse and forcing a new debate. Innovation is making it possible—and necessary—to rethink how best to protect people amid new options, opportunities, and risks.

For a moment, imagine this future:

Consumer: “I need a new credit card.”

Consumer’s phone: “Since you pay your full balance every month, interest rates won’t matter. But you occasionally pay late, so I’ll check penalty terms, and I know you want travel rewards. I’ll also exclude anything with hidden fees or bad terms. Okay. I suggest these two cards. The first has better customer ratings and complaint scores. Let’s discuss them.”

Questions prompted by this exchange could fill an article. Bankers should be asking them now. Four big tech trends, while intertwined, have not converged. When they do, the impact will be explosive. The four trends are big data, artificial intelligence, natural voice technology, and mobile. (Just behind them, arguably, is another: cryptocurrency.)

1. BIG DATA

Big data is rapidly changing everything—not just banking. Industry now gleans information from social media, GPS locators, government websites, and the “internet of things.”

IoT links the computers embedded in smart devices around us—not just phones, computers, and tablets, but cars, cameras, TVs, electronic keys, thermostats, baby monitors, and more.

I had a health issue last year, and while my medical records have privacy protection, it would be easy to guess at my situation based on what I was Googling. Our devices increasingly “know” our tastes, locations, and routines, and, increasingly, use facial recognition technology to assess if we like what we see.

Meanwhile, government records are being digitized and shared with API (application program interface) formats, making them easy to access and use in new ways. CFPB’s complaint portal and Home Mortgage Disclosure Act repository—and its coming database on small business lending—are a few examples.

Big data carries huge upside potential and also risks for consumers. Industry can use data-driven insights to customize offerings and widen services for consumers lacking conventional credit profiles. The same technology empowers consumers to find and evaluate good options.

These trends raise concerns about privacy, data security, and fairness of data use. Big data is notoriously inaccurate and hard to manage. Much is collected for purposes that don’t require accuracy—until information is put to new uses, driving decisions that can harm consumers.

2. ARTIFICIAL INTELLIGENCE

Artificial intelligence adds to the upside and downside potential of big data by leveraging it for new uses.

Today, a machine can be given a question and then search all the digitized information in the world. The computer observes things; guesses at what might be useful; brings this back for feedback; and then uses this to improve—endlessly.

Goldman Sachs’ Kensho can answer millions of complex investor questions in plain language, and even predict how types of stock would perform in various scenarios. An IBM supercomputer has graduated from chess to inventing recipes that maximize flavor and nutrition.

In medicine, machines not only read radiology reports, but foster cancer research by “noticing” patterns no one even told them to look for. All this is incredibly fast and increasingly cheap.

3. NATURAL VOICE

Artificial intelligence links to the third breakthrough underway, natural voice technology. Computers already translate between voice and text, and between languages—even mimicking speaker voices.

Meanwhile, phone concierges like Apple’s Siri and Microsoft’s Cortana can make reservations and handle fact queries like: “Where’s the nearest gas station” or “Who was the third U.S. president?” And Amazon’s Alexa executes action requests like turning up the thermostat as we head for home.

Those services, however, have been mainly about handling facts and carrying out human decisions, and summoning information and translating it from and to voice. The new development is that voice technology is now using neural networks and deep learning to listen and then “think,” so that machines can converse with us in a natural dialogue.

This trend is likely on a slower path than the first two trends, but its implications for financial services are profound. Millions of consumers who are uncomfortable reading financial material will find themselves able to get clear information and make good choices by having a conversation with their phone.

4. MOBILE SERVICES

That brings us to the fourth trend, mobile, and maybe the one whose impacts are hardest to envision.

To financial services people, mobile is a payments topic, and, of course, payments is a financial topic. That underplays what is happening. It is true that mobile payment—scanning a phone at checkout instead of using cash or cards—is growing. Apple Pay, introduced last fall, is catalyzing growing acceptance by merchants, consumers, card issuers, and banks, which is generating more competition from mobile payment providers like Google, with its new Android Pay.

That trend coincides with another—the so-called “uberization” of payments. Companies are working toward the goal of making the payment process disappear into the consumer experience—just as a passenger exits an Uber car with no exchange of money or documentation, since those have already been prearranged electronically. As more payments are handled this way—and as payment technology increasingly permits skipping the checkout counter—consumers will be encouraged to spend more, a trend that will concern regulators and advocates.

The same concerns will be fueled by geolocation technology, which will spur more spending by alerting us to attractive buying opportunities nearby.

At the same time, though, these mobile technologies can be turned around and used to empower people to manage their financial lives more mindfully.

Once the phone becomes a primary financial tool, it will start managing our money lives. Suddenly, people’s financial information will be easy to consolidate (most banking is already online), instead of coming in fragmentary forms.

It also will always be current. Already, innovators are creating powerful new apps to make it easy and effortless to track spending and to save without budgeting effort. Behavioral science is learning how to connect our financial habits with our emotionally cherished life goals, and to use research-proven motivators, like lottery-style rewards, to help people save.

All this will transform habits. Our phones will “nudge” us against overspending: “We’re near Starbucks, but you’ve spent $23 there this week! Shall I put the price of the latte into the college fund instead?”

Our new behaviors will inspire Amazon- and Yelp-type marketplaces and product ratings as innovators tap into big data, including government complaint repositories, to create easy and automatic rankings and recommendations.

Our phones will be able to sort choices and actually block out those with hidden danger. Businesses that rely on obscure fees or tricky terms will find their profit models in trouble as innovative, affordable offerings proliferate from banks, technology giants, and startups to help consumers avoid pitfalls.

One more impact of mobile: It will greatly expand financial inclusiveness. Importantly, lower-income people are disproportionately high users of smartphones, including for financial tasks. This is partly because many never had good access to the more expansive online banking that uses a PC and broadband. That fact, and mobile systems’ low cost, will help expand services for the 70 million Americans struggling for access.

The phone is changing how people interact with the world. Banking is just one part of the new ways to manage life.

Convergence is coming

The fifth big trend is digital currency, or cryptocurrency. Whatever the future of Bitcoin, the invention of the blockchain as a distributed ledger that is open, online, instant, transparent, verifiable, and cost-free will massively remake not only payments, but systems ranging from stock markets to legal records.

As these trends converge, financial education will leap from the classroom to our phones, tablets, and wearable devices—when we want it and in forms that are simple, personalized, and even entertaining. If you don’t want your financial coach to have the personality of MeetCARROT, you can have one that is a friendly puppy or neighborhood banker.

Josh Reich, CEO of online bank Simple, points out that the automatic transmission made it possible for people to drive without really understanding how a car works. Financial services is headed to a similar democratization.

Bad, ugly accompany good

Let’s not forecast a dystopic future, but let’s be realistic. Even today, myriad examples of technological abuse have been seen. Every one will bring problems as well as benefits:

• Consumer confusion will rise before it falls—and it will be exploited.

• Bank branches will decline and be repurposed, frustrating many older and lower-income customers.

• People will overspend. Some consumers will rely on new phone tools that conceal flaws and bad motives. Developer “bias” may be something people will question.

• Privacy, data security, and basic fairness will be constantly threatened.

Should your loan cost more because you “like” certain things on Facebook or have “too many” social media friends? Such questions will test legal norms.

These challenges will overwhelm traditional regulatory structures and methods, especially those that are bank-centric.

The new market will be less about banking and more about new consumer tools and behaviors. In fact, banks will face extra problems because, being so highly regulated, they will likely be held to higher standards and forced to retain old methods longer, such as expensive delivery channels like branches.

Nimble, efficient, “cool” new competitors, meanwhile, will snap up market share. Google, Facebook, Amazon, and Apple already offer financial products in some form. They have massive channels and consumer bases. And some of them are liked—even loved—by customers. This points to another whole realm of disruption around the roles and even the meaning of the bank charter.

What’s a bank? A regulator?

Banks, increasingly, will enter into relationships with nonbanks in many innovative areas. Likewise, banks will find third parties inserted between them and their customers, whether the bank is actively partnering or not.

How will this impact both business and regulations? How will disclosures have to change? Who will be responsible for data security? Are the regulators—increasingly focused on vendor relationships over the past few years—worried about the right things?

The new technology will flow around fragmented agencies, including the CFPB, and lead to consequences like:

• Regulators enforcing obsolete disclosure rules, while people just pull out their phones for financial guidance.

• Government attempts to curb any harmful change will accidentally kill off good innovation.

• Countless small developers will launch new financial apps, blithely unaware that regulations even exist.

The coming changes raise bedrock questions. Among them: Who among banks, big technology firms, startups, independent rating entities, or government agencies reliably protects consumers? And what will happen when businesses know everything about us, but we also know everything about them?

As banks tackle these challenges, they will have to combine their regulation and innovation work.

Building consumer protection into every innovation decision, regardless of whether or not there is a regulatory rule to follow for it, is about to become a new survival skill.

In the end, innovation and technology have set off a new contest. The stakes: Who will win consumer trust?

This article originally appeared in the July 2015 print and digital edition of Banking Exchange magazine.

Tagged under Mergers Acquisitions; Financial Trends; AI; CSuite; Feature; Feature3;