How Community Banks Go Public

Understanding the capital, regulatory and investor needs will allow a community bank to determine the best way forward

- |

- Written by Laura Hamilton, OTC Markets Group

For many community banks, going public is the next logical step in their growth trajectory and can provide a better, easier way to gain access to the capital needed to support their local economies. But HOW banks go public often will depend on the individual characteristics of the bank. Understanding the capital, regulatory and investor needs will allow a community bank to determine the best way forward on its journey into the public markets.

Today, a community bank has three options to offer their stock to investors. Depending on who you speak with, the BEST path to the public markets varies. It has been my experience that those bank executives who take the time to thoughtfully evaluate their options and map the process of going public to their long term goals seem to produce the best results -- for the bank, for its customers and ultimately for its shareholders.

Capital Needs

While going public can fulfill existing capital needs, a bank should also consider how these needs will change over time and potentially be different after going public. When looking at the allocation of capital post going-public, banks need to consider the increased cost associated with running a public company. These include, but are not limited to, an increased workforce to manage investor relations needs as well as a deeper bench in the financial reporting and accounting teams.

Additionally, the amount of capital a bank currently has may determine whether the bank chooses to IPO on an exchange (NYSE or Nasdaq), or considers a more cost-effective option via a Slow-PO on OTC Markets Group’s OTCQX Market. Generally speaking, if a bank is looking to raise a significant amount of capital, they’ll look to conduct an IPO onto an exchange. If a bank is simply deciding to make its shares available to the public market, without a capital raise, then they would opt for a Slow-PO (similar to a direct listing) on the OTCQX Market.

A traditional exchange IPO requires that a bank be SEC filing and typically entails a 12-24 month planning process. Trading on OTCQX requires that a bank meets high financial standards, including having at least $100 million in total assets and at least 50 beneficial shareholders to qualify, and is often less burdensome and more affordable than the exchange route.

We explore the following options and what community bank executives should consider as they evaluate each one:

- Desk Drawer

- “Slow-PO” (via OTC Markets Group)

- IPO via a national exchange

The Desk Drawer

Look inside the “desk drawer” of many, if not most, community bank presidents and you will find a list of the names of individuals who want to buy or sell the bank’s stock. Generally speaking, a desk drawer transaction is a private stock sale brokered through the bank CEO or CFO to existing shareholders of the bank. These transactions are common practice among hundreds of private community banks nationwide and serve their purpose well.

That said, as a community bank continues to experience growth, desk drawer transactions could begin to pose a legal risk to even the most scrupulous and careful presidents who administer them. Transactions from the desk drawer should remain occasional and isolated. If the practice becomes commonplace, and a bank is confronted with investors looking for more frequent stock transactions -- either to purchase more stock or liquidate their position -- this may signal it is time to evaluate whether a better, safer system exists, such as the over-the-counter market.

The “Slow-PO”

A “Slow-PO" allows an efficient entry point to build investor confidence and liquidity organically, by making previously restricted shares available for public trading by brokers on OTC Market Group’s OTCQX®, OTCQB® and Pink® markets.

Akin to a "direct listing" on an exchange, during a Slow-PO a company goes public without raising money and without underwriting as in a traditional exchange IPO. However, a bank can still raise capital via a Regulation D or Regulation A offering, prior to a Slow-PO. The longer on-ramp via a Slow-PO allows community banks with an established, existing investor base to avoid the complexities, distraction, expense, time pressures and uncertainty of a traditional IPO, while growing their liquidity organically over time. This frees up time for banks executives to focus on executing their business plans as they manage the trajectory to grow into the bank they aspire to be. We continue to hear from bank presidents that the Slow-PO achieves the liquidity community bank investors need, providing a growth opportunity to attract new investors to the stock, while not overburdening the bank’s operations team.

The Exchange IPO

Entering the public markets via a national exchange can be both expensive and quite burdensome, but to some community banks this remains the end goal. A community bank that seeks to sell its stock on the Nasdaq or another national exchange faces more onerous listing requirements. The costs of the IPO itself are steep, with a large team of consultants, attorneys and investment bankers to engage. Additionally, the underwriting, legal and accounting fees to go public are significant. According to a PwC survey, 83% of CFOs estimated spending more than $1M on one-time costs associated with their IPO. In contrast, a direct listing is much more cost effective.

In speaking with hundreds of community bank presidents over the years, I continue to hear them conclude that the market or exchange in which their stock is traded isn’t as important as the function the public markets provide. Carefully balancing those factors with the cost and resources for each option will result in the best decision for the bank, its investors and the community.

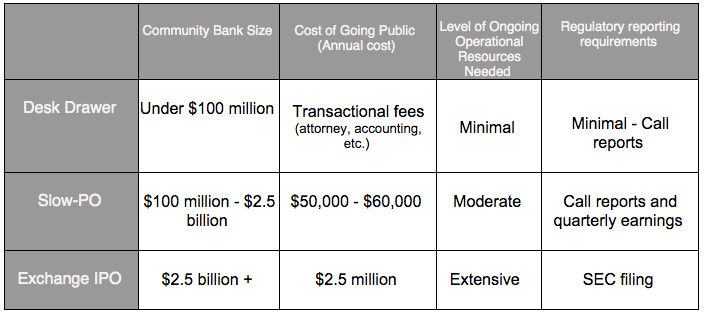

The chart below provides a starting point when evaluating the three routes to IPO detailed above. While each bank is very different and there are MANY exceptions to each of these scenarios, private banks should take the following factors into consideration when looking to go public.

Laura Hamilton is a Vice President at OTC Markets Group where she manages the Community Banking Group for the U.S. Laura has advised over 125 community banks that trade on OTCQX Banks on trading and liquidity in the U.S. Equity Markets. Connect with Laura via LinkedIn.

Tagged under Community Banking, Feature3, Feature, Management,

Related items

- Banking Exchange Hosts Expert on Lending Regulatory Compliance

- Merger & Acquisition Round Up: MidFirst Bank, Provident

- FinCEN Underestimates Time Required to File Suspicious Activity Report

- Retirement Planning Creates Discord Among Couples

- Wall Street Looks at Big Bank Earnings, but Regional Banks Tell the Story