5 Ways to Overcome Lending Inefficiencies to Prepare for Economic Uncertainty

The coronavirus has sent shockwaves through the markets around the globe

- |

- Written by Kylee Wooten, Abrigo

The coronavirus has sent shockwaves through the markets around the globe. To mitigate disruption to the economy, the Federal Reserve made its second emergency cut to interest rates on Sunday, marking the largest emergency reduction in the Fed’s history. Low interest rates and slowing growth in loan demand can put community financial institutions in a difficult position. Becoming more efficient and mitigating any increased risk should top the priority list for community financial institutions across the country.

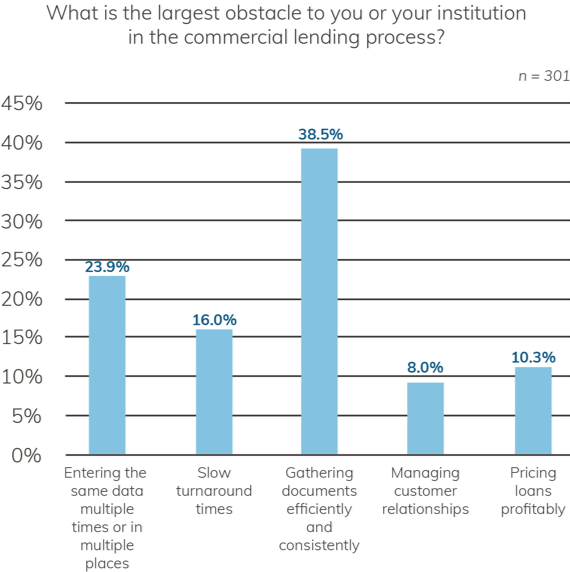

Abrigo’s 2020 Business Lending Readiness Survey identified a number of pain points that thwart business lending growth, from document gathering to lengthy loan turnaround time. Here are the top five inefficiencies holding community financial institutions back and how to overcome these challenges to stay effective in an uncertain economic climate.

Wrangling documents

One of the largest obstacles to the commercial lending process, according to respondents, is the ability to gather documents efficiently and consistently.

A key contributor to this issue is the lack of a clear, consistent credit policy. “The more leeway there is, the higher the likelihood that staff will need to go back to the borrower for information,” said Alison Trapp, Director of Client Education at Abrigo.

Community financial institutions should develop a clear credit policy outlining expectations and application requirements. Community financial institutions may also consider leveraging technology to make it easier to collect and track documents, as well as notify borrowers of missing items.

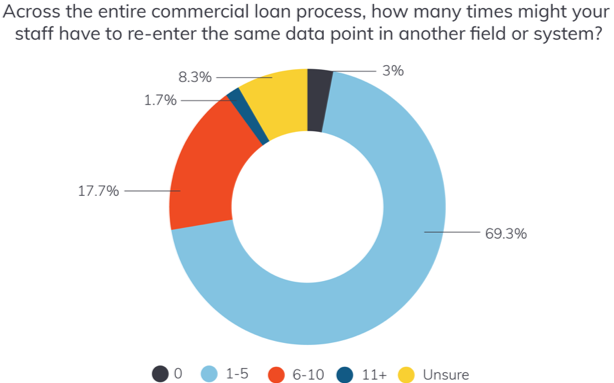

Manual data entry

When financial institutions use disparate systems, staff must repeatedly enter the same information, wasting time and risking costly data entry errors. Eliminating data re-entry should be a top priority for institutions that want to save as much time as possible and eliminate unnecessary risk.

Online loan applications can reduce the back and forth to help manage the document gathering process, as well as eliminates data entry for lenders. Financial institutions benefit from a single point of data entry, where that information can easily flow through to other applications, such as financial spreading and analysis, rather than being entered manually in another system.

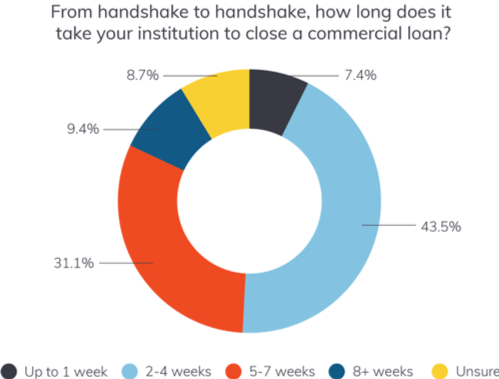

Slow loan turnaround

Wrangling documents, manual data entry, and other inconsistent and time-intensive processes make it difficult to get an answer back to borrowers or members quickly. Only 7% of respondents said that their institution could turn around within a week.

To solve this issue, community financial institutions are turning to automation. Automation can prepopulate fields and trigger notifications so nothing falls between the cracks. Furthermore, automating the workflow can help streamline and track the progress of the loan by using notifications to prompt next steps, reduce bottlenecks, and document the process for better auditability.

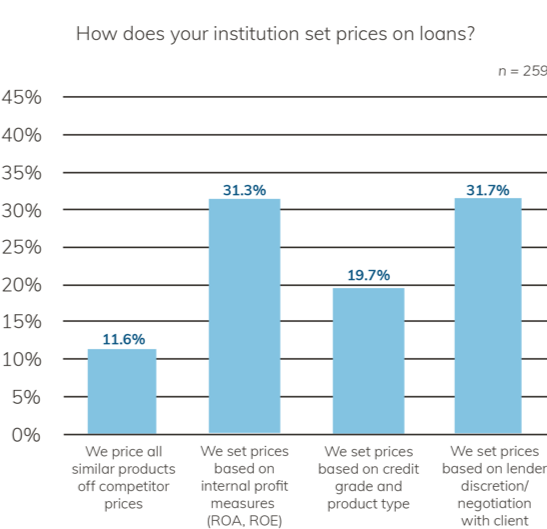

Pricing loans profitably

Financial institutions – community financial institutions in particular – walk a fine line with loan pricing. On the one hand, institutions want to be competitive and earn more business; on the other hand, institutions must manage risk and price loans according to the risk that they are taking on.

The largest group of respondents answered that they set prices on loans based on lender discretion and client negotiation. This is concerning to David O’Connell, Senior Analyst at research firm Aite Group, who noted that the margin for error on loan pricing is “almost nil” with spreads so thin right now.

In this increasingly competitive environment, and uncertain economic conditions ahead, banks and credit unions must make informed pricing decisions that accurately capture costs of administering the loan and assuming the risk of the borrower or member. Today’s technology allows financial institutions to integrate loan pricing, credit analysis, and risk rating software to save time, improve efficiency, and quickly generate reports to justify pricing decisions.

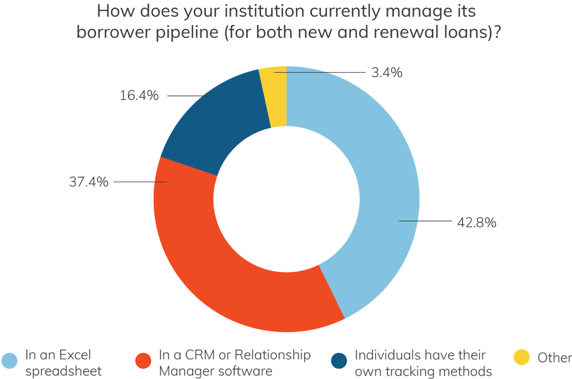

Managing customer relationships

Over half of respondents reported managing the institution’s borrower pipeline through Excel spreadsheets or using individual tracking methods. These approaches miss out on vital management information.

“You need operational analytics,” O’Connell said. “You want to know things like, how long is it taking us to do a CRE deal? If it’s two weeks longer than C&I, that makes sense. But maybe you’ve got one team of lenders closing loans 1.5 weeks early, and maybe they’ve got underwriters embedded in their team. If you’re [managing the pipeline] in Excel, you’ve ceded the opportunity to do operational analytics.”

For greater operational analytics and transparency into the borrower pipeline, financial institutions are using relationship manager technologies that aggregate all customer information into a 360-degree view of each customer and loan. This technology helps financial institutions to centralize all customer engagements, accurately report on the institution’s lending pipeline, and track all open opportunities.

Community financial institutions have no control over the economy. However, by examining key inefficiencies and processes that add costs, delay turnaround times, and increase risk, financial institutions can be more prepared for economic changes and remove obstacles to success.

Kylee Wooten, Abrigo