Curtain rises on CRA reform

Treasury involvement could be catalyst to bring regs into 21st century

- |

- Written by Steve Cocheo

As Community Reinvestment Act regulatory reform begins to take shape, the Treasury Department appears to be taking a greater role in the process than is typical.

As Community Reinvestment Act regulatory reform begins to take shape, the Treasury Department appears to be taking a greater role in the process than is typical.

Impetus for reform of Community Reinvestment Act regulations—not updated substantially since 1995—is beginning to warm up. If history, and Washington mechanics, are any guide, the process isn’t even at the end of the beginning, but momentum appears to be building.

Back in June 2017, in a major white paper on financial services reform, the Treasury Department briefly targeted CRA rules as an area in need of updating, rethinking, simplification, and clarification. The report, A Financial System That Creates Economic Opportunities, indicated that “aligning the regulatory oversight of CRA activities with a heightened focus on community investments will be a high priority” for Treasury Secretary Steve Mnuchin. Early on, Comptroller of the Currency Joseph Otting made it clear that CRA regulatory reform was a top priority of his, as well.

On April 3 Treasury dropped the other shoe, with a 35-page memorandum to OCC, the Federal Reserve, and FDIC setting out the department’s priorities for CRA reform. (The Consumer Financial Protection Bureau has no direct role in CRA, and credit unions are not covered by the law.) In part this drew on input that Treasury received from nearly 100 players from all sides of the CRA debate.

Treasury’s recommendations to the regulators fall into four major categories: CRA assessment areas; examination clarity and flexibility; the examination process; and performance evaluation and ratings. Each of these is covered later in this article.

What other regulators are saying

In press meetings and an interview with Banking Exchange earlier this year, Comptroller Otting has spoken at length about the broad outlines of his ideas on CRA regulatory reform, and about the reactions various interests have had to his ideas.

When Treasury’s memo came out, OCC (a part of Treasury) confirmed that it continues, in consort with the other agencies, “to prepare an Advance Notice of Proposed Rulemaking that will be released soon to solicit stakeholder comment on improving how CRA is implemented to better achieve its original purpose of encouraging banks to meet the credit needs of their communities, including in low- and moderate-income (LMI) neighborhoods, consistent with the safe and sound operation of such banks.”

OCC’s spokesman said comments reacting to the advance notice would be used to develop a more specific policy proposal later in 2018, likely in the form of a Notice of Proposed Rulemaking.

In mid-April, two members of the Federal Reserve Board commented on reform—one an Obama appointee and the other a Trump appointee.

In an April 17 speech, Fed Governor Lael Brainard endorsed the general idea of reform.

“The time is ripe to modernize the CRA regulations to make them more effective in making credit available in low- and moderate-income areas at a time when technological and structural changes in the banking industry allow banks to serve customers outside of areas with branches that have traditionally defined a bank’s community,” said Brainard.

One concern she raised in her speech was that reform should address the challenge of “credit hot spots.” These are markets with a high proportion of banks relative to investment opportunities, as opposed to markets with sparser banking services that have trouble attracting capital.

Brainard also favors tailoring CRA regulation to bank size and business strategy.

“Regulatory revisions that do not contemplate evaluating CRA performance in context risk undermining CRA’s greatest attribute—its recognition that banks are uniquely situated to be responsive to the most impactful community and economic development needs in communities,” said Brainard.

Randal Quarles, the new Fed vice-chairman for supervision, in congressional testimony given the same day, said in response to a question that he felt both banks and regulators had to “move off autopilot” in CRA compliance. He reportedly praised Treasury’s memo—not surprisingly, given that he is the Trump appointee of the pair.

Eugene Ludwig, founder and CEO of Promontory Financial Group, who was Comptroller of the Currency during the last round of CRA reform in 1995, says the timing of looking at CRA reform is appropriate. “Asking many of these questions about CRA’s efficacy is the right thing to do,” he said. Ideally, the regulations should be reviewed about every five years, he said, in a “refresh cycle” to account for changes in the banking industry. He said that the reform he helped squire to reality made the rules more efficient and effective for their time, but much has changed.

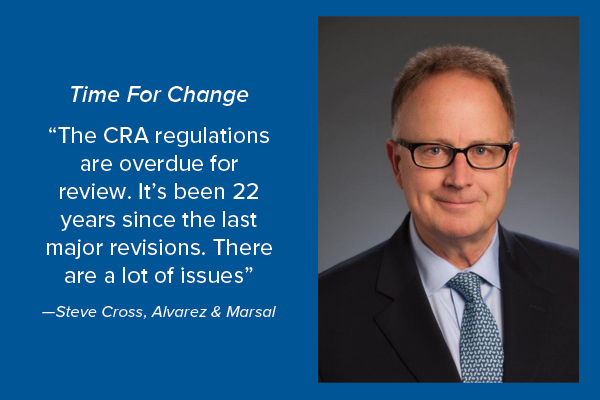

Stephen Cross, now senior advisor with Alvarez & Marsal with a specialty in CRA, also served at OCC— as deputy comptroller for compliance—during the period that the regulations were revamped. He agreed the push for reform is timely. In fact, he said, “I think CRA regulations are overdue for review.”

“It’s been 22 years since the last major revisions,” Cross said. “There are a lot of issues.” How to handle compliance for banks with nationwide footprints, for example, is only one factor that wasn’t resolved in the mid-1990s, Cross said.

Role of Treasury in reform

It’s not unusual for the Treasury Department to be involved in financial policymaking. Nevertheless, the degree to which Mnuchin’s Treasury is driving thinking about financial services policy is strong, and with the memorandum to the regulators about CRA, a bit unusual in its detail.

During a session about deregulation efforts under the Trump Administration at the recent LendIt Fintech conference, Jonah Crane, a panelist, told of being in a meeting about financial policy issues with a group of regulators recently.

“To a person, they said, ‘Let’s see what Treasury has to say’,” according to Crane.

He remarked that he and a colleague found that amusing. Crane, now executive director of RegTech Lab, served as a senior advisor at Treasury during the Obama Administration, and prior to that as a policy advisor to Sen. Chuck Schumer.

“The regulators never cared what we said when we were at Treasury,” said Crane. But he said that the change from the Obama regulatory cadre to the Trump team has not been a normal transition, so colored has it been by the urge to roll back many aspects of the Dodd-Frank Act.

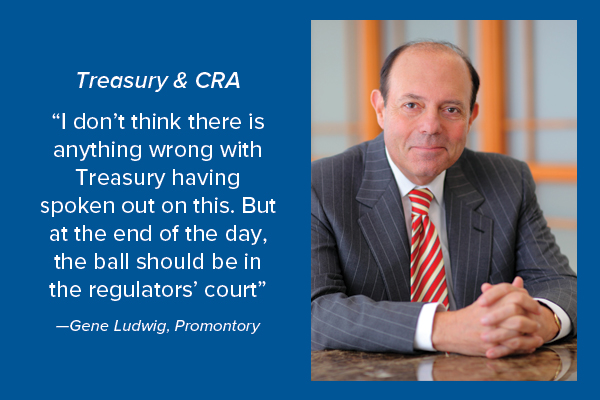

“I don’t think there is anything wrong with Treasury having spoken out on this,” said Gene Ludwig. “But at the end of the day, the ball should be in the regulators’ court.”

Who’s in charge? It’s been an interesting dynamic to watch, according to Krista Shonk, vice-president, regulatory policy, at the American Bankers Association. She said it would be best for the industry if the regulators can work together to produce joint rules, for the sake of consistency. Shonk said the industry wants reform, and generally likes the direction of the Treasury report, but it would sacrifice earlier reform, if necessary, for the sake of uniform rules.

Timing of reform is an open question. There is a sense of urgency—Otting has pointed out that regulators, activists, and bankers all dislike CRA as currently administered. However, Washington only moves so quickly under the most ideal conditions. Shonk said that originally common wisdom indicated that the Comptroller’s Office would have its own Advance Notice of Proposed Rulemaking out in March, but then indications were that the hope was to make the document an interagency one. (Jelena McWilliams, a banking attorney nominated for the FDIC chairman’s post, has been confirmed at the committee level but not yet by the full Senate. That confirmation may play a part in the timing of the CRA issue.)

“If there were to be an interagency ANPR,” said Shonk, “that would be better for all stakeholders.”

“After all is said and done,” Shonk added, “it’s going to be a multi-year project.”

Indeed, the 1995 regulations mostly became effective in July of that year, about two years after President Clinton tasked the regulators with revamping the rules.

Wary of credit allocation

“Transparency” is one of those buzzwords that mean different things to different people, and sometimes the meaning hinges on which side of an issue one sits on. In the Treasury memo, the theme of transparency comes up in multiple places, as does the theme of clarity.

Gene Ludwig understands the desire for greater transparency in CRA regulation and examination. “The world we live in is a world of greater transparency,” he explained. “Examinations tend not to be transparent.”

ABA’s Krista Shonk gives an example of the sort of transparency that banks would find helpful. A common frustration among them, she said, is that examiners have access within their agencies to online bulletin boards where they can keep up to date remotely with issues such as CRA examination developments. While examiners can tap this resource, she said, banks can’t see the data.

Major portions of banks’ CRA exam reports, including the final ratings, can be accessed online by anyone, but those would have to be studied in depth to gain the same kinds of insights. That said, Shonk makes the point that CRA exams involve a good deal of examiner discretion. One of Comptroller Otting’s particular desires, expressed during the interview with Banking Exchange, would be finding a way to bring CRA evaluation down to some type of performance measurement based on hard metrics.

Ludwig acknowledged that bankers typically like the idea of “bright lines” showing definitively how to be in compliance, but they also crave flexibility in complying. “I do think that everyone benefits from focusing on transparency,” said Ludwig. However, both he and Steve Cross pointed out that there are two sides to being more explicit.

The “dark side,” if you will, about explicit standards is the risk of credit allocation, something that bankers have resisted, historically. “That’s the reason why our final reform regulations weren’t more quantitative in nature,” said Ludwig. Going beyond the points in the 1995 rules would have led to the political quagmire of potential credit allocation.

“We’re concerned about the notion of federally mandated quotas,” said ABA’s Shonk. There’s a balancing act between coming up with a simplified measurement and the risk of a threshold that becomes a “line in the sand” that doesn’t capture the full picture of a bank’s CRA activities, she said.

Looking at some specifics

Major bills as introduced, government policy papers, and first versions of new regulations notoriously bear only some resemblance to final products in Washington. However, at this point the Treasury memo is the most concrete document pulling together potential revisions, so it is worth a look at a few highlights of what was recommended.

Assessment areas. Ultimately, how a bank’s performance is measured hinges on how the assessment area is outlined. This is the geographic area it is considered to be serving. The report notes that as the industry’s structure and approaches have evolved, the significance of assessment areas has as well.

“Treasury recommends revisiting the approach of determining assessment areas,” it stated in the memo. “CRA’s concept of community should account for the current range of alternative channels that exist for accepting deposits and providing services arising from the ongoing evolution of digital banking.”

Examination clarity and flexibility. This is an extensive section of the memo.

A key matter considered is what qualifies for CRA credit, among loans and investments. The memo recounts how agencies formerly gave written, public determinations when questioned regarding qualifying efforts.

“Currently, there is no formal process available to aid in the determination of whether a loan or investment will qualify for CRA credit,” the memo states. The memo calls for expanding qualifying loans, investments, and services, and setting up clearer standards of eligibility for CRA credit, with “greater consistency and predictability across each of the regulators.” Treasury also spoke of its support for “any reform effort that embraces innovative approaches to CRA eligibility definition, including technology-enabled approaches.”

While acknowledging that questions come up, Cross said that “I’m not sure the problem is as bad as the Treasury people make it out to be.” He said Q&As that have been issued, as well as other guidelines, make it clear in his mind what qualifies. He thought some expansion could take place, to facilitate financing of infrastructure projects.

Another issue concerns “performance context.” These are factors that give an examiner a sense of the environment in which a bank’s CRA efforts are made. These include, as listed by Treasury, “demographic and economic data; community-specific insights relating to the lending marketplace; investment and service opportunities in the assessment area; the bank’s product offerings and business strategy; and the institutional capacity and constraints of the bank that affect its ability to respond to the needs of the assessment area.” Public comments, performance of peer banks, and the bank’s own past CRA efforts are also weighed.

In its recommendations in this area, Treasury states that it believes that “CRA regulation has too many subjective elements. This creates significant compliance burdens and related costs, without any commensurate gain in quality or execution of banks’ CRA activity in the communities that banks are aiming to serve.”

The department recommends that regulators use their own research and policy staff to better develop performance context in advance of exams, in part to remove some burden from exam staff.

Treasury also wants to see a revamped viewpoint on the service test element of CRA exams. “The ongoing adoption of alternative delivery channels will continue to lessen the relevance of physical branches to all communities, including LMI communities, over time,” the memo states.

Examination process. In tables published in the memo, Treasury makes the point that while the three prudential regulators work from the same CRA regulations, they maintain differing examination schedules. These vary by the institution’s previous rating and by bank size, but can range from 12 months since the most recent exam to 72 months. In some categories, agencies differ by years in how often they’ll come back. Treasury wants to see this standardized across the agencies.

CRA performance. A key point in this section—as well as the previous one—is the delay in releasing exam findings.

“Banks and community and consumer advocates suggested that the amount of time that it takes to conduct CRA examinations and to disclose CRA performance evaluations publicly has become excessively long,” Treasury stated. “…This leaves many banks with dated ratings. Further, delays in the release of performance evaluations can result in minimal time for a bank to respond and react to recommendations prior to the commencement of their next performance evaluations.”

“I think that that is a legitimate issue,” said Stephen Cross, former deputy comptroller, “but there are two sides to that issue.” Cross explains that, given how much of a CRA exam report is made public—even the bank’s rating—regulators routinely give the banks an opportunity to react to draft reports. This assures that there will be delays, he said.

Cross added that if a potential fair-lending issue comes up—it’s a factor that CRA examiners consider—this can also delay a CRA exam report significantly. Fair-lending issues can take a long time to investigate and finalize, said Cross.

For its part, Treasury acknowledges such reasons, but thinks reports shouldn’t be delayed by pending investigations. If an investigation produces evidence of discrimination or other illegal credit practices, it states, this could be handled by making an addendum to the CRA exam report.

Financial education

One element of the memo that stands out is a page-size addendum about CRA and financial education—it’s the only place the matter is touched upon.

“There is generally agreement that the CRA regulators should provide greater guidance on how these activities will be considered under the Service Test and that guidance should encourage banks to support high quality financial education that leads to real impacts,” the document states.

Further: “Banks should be encouraged to partner with and invest in professional experts who could deliver these services, rather than simply relying on existing bank staff.” This is interesting, in that banking associations have often emphasized bringing bankers into schools, and more, to give a real-world view of financial management, rather than the bank paying someone else to provide such education.

Over the years bankers have sometimes complained that their efforts to provide financial literacy training in schools were stymied by teachers’ unions, which resisted having non-members in classrooms.

Overall, ABA’s Shonk said that this segment of the memo is of some concern. At present, she said, ABA members have spoken of the challenge of proving to regulators that their outreach efforts in schools assist low- and moderate-income households. They can make the effort, but credit isn’t always granted.

“It makes you head hurt,” she said, “to hear banks talk about this.”