Long and short of liquidity

Sound liquidity management can also improve earnings. Stress testing, contingency planning prove essential

- |

- Written by ALCO Beat

ALCO Beat articles featured exclusively on bankingexchange.com are written by the asset-liability management experts at Darling Consulting Group.

ALCO Beat articles featured exclusively on bankingexchange.com are written by the asset-liability management experts at Darling Consulting Group.

By Zach Zoia, consultant, Darling Consulting Group

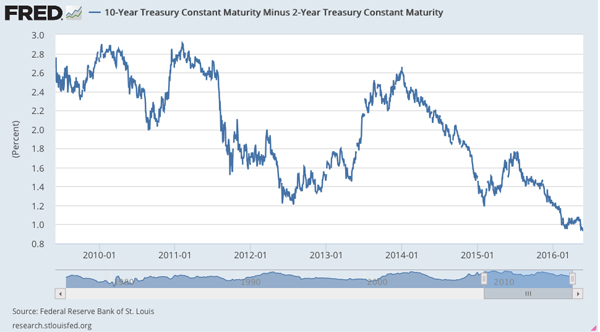

One-hundred basis points. That is the approximate spread between the 2- and 10-year points on the Treasury curve. Roll back the clock to the start of 2014 and that same spread was north of 250 basis points.

This flattening of the yield curve continues to exert pressure on net interest margin (NIM) throughout the industry. Asset spreads are narrower. Pricing pressures on funding costs are being seen. And, with net interest income (NII), a function of NIM, typically comprising the majority of income earned in the community banking space, the current yield curve is problematic.

Facing pressure to preserve margin, institutions around the country have been growing their balance sheets; shifting their asset mixes more toward the higher-yielding loan portfolio; and/or utilizing the wholesale funding markets to more cost-effectively manage deposit volatility and support asset growth.

Since 2012, loan-to-deposit ratios at community banks (between $100 million and $10 billion) increased from 78% to 84%. And wholesale funding levels—including brokered deposits—rose 35%.

While these strategies can help improve NII levels, they tend to use previously unencumbered liquidity sources. As the current rate environment does not appear to be abating anytime soon, a strong understanding of your institution’s liquidity position is critical to executing future strategies that your ALCO develops to maintain, or grow, margin.

Proactive measurement and management of liquidity is critical in the challenging current rate environment. A strong and diversified liquidity profile will bring your bank both flexibility to manage future asset growth plans and better control the cost and stability of your funding base. Liquidity management—like interest-rate risk measures and earnings, is crucial for optimizing balance sheet performance.

Let’s begin with a series of questions that, though they may sound basic, may remind you of fundamentals that have been blurred in today’s unusual times.

What is liquidity?

One definition is the ability to generate cash quickly, at reasonable cost, without loss of principal.

Within this, “quickly” should encompass a 30-day window; “reasonable cost” means current wholesale market; and “without principal loss” implies that there is no need to sell assets in order to generate cash.

Inherent in this definition: Liquidity means more than just short-term cash equivalents or investments with maturities in the next 12 months. Understand also that raising cash should not require liquidation of assets nor premium rate deposit special offerings.

Key components to optimally satisfying the above definition are the levels of free bond and loan collateral that can be used to secure future borrowings (i.e., access to cash), as well as the ability to access funds in the brokered market.

What are liquidity’s components?

The first layer should be represented by “on-balance sheet” liquidity. It includes, among other items, excess interest-bearing cash; other short-term liquid assets; and unencumbered agency-backed bonds.

The ability to borrow against bond collateral is an important element of the calculation. That option enables an institution to maintain liquidity while optimizing the yield in its investment portfolio (i.e., no requirement to hold a high level of cash).

The accounting designation on your bonds—“available for sale” or “hold to maturity”—is immaterial, because it is not necessary to actually liquidate the holdings to generate liquidity. And these bonds can be pledged against a variety of potential funding resources.

However, one caveat: Collateral values may change with movements in interest rates, which could, for instance, reduce the potential amount of liquidity that can be accessed in a rising rate environment.

Understanding the market value impact is part of contingency planning and stress testing, which I’ll address in a moment.

The next component in a liquidity plan is a “just-in-time” inventory, or loan-based borrowing capacity at the Federal Home Loan Bank (FHLB). Pledging loans to the FHLB affords the ability to transform a generally “illiquid” asset (e.g. 30-year residential mortgage) into a vehicle which allows a bank to obtain short-term funding for day-to-day liquidity management—or extend into longer-term funding, if necessary, depending on interest rate risk profile.

Further, wholesale markets provide another funding alternative in the form of brokered deposits, which comprises a third tier of liquidity, or “strategic reserve.” Well-capitalized institutions are typically able to access this facility under a board-authorized policy.

FHLB borrowings and brokered deposits are important aspects of a comprehensive liquidity plan. These resources, relative to retail deposits, are available in bulk; can be accessed quickly; and are stable. Also, they do not lead to cannibalization within the current deposit base nor to a higher marginal cost of funds like a high-cost special could.

These three components—on-balance-sheet liquidity, FHLB advances, and brokered deposits—comprise an operational level of liquidity which allows an institution to access a diverse set of funding alternatives without having to hold excess balances of minimally yielding cash or to pay premium rates for deposits.

Avoiding those actions proves especially critical in the current rate environment when earnings are being challenged.

For example—assuming this fits the interest rate risk profile—a transaction whereby excess cash is deployed into mortgages could net an additional 300 basis points of spread while only reducing overall liquidity by a factor of 25%.

Here’s the reasoning behind that statement: Residential mortgages earn a return, yet they can be pledged to the FHLB at approximately 75% of the collateral, if need be. That’s only a 25% disadvantage to cash, which would be 100% available.

What about longer-term forecasting?

The approach described above relates to an analysis over a 30-day timeframe. Naturally, effective liquidity planning needs to extend well past 30 days. How far?

Once you understand your current liquidity position, layer in the effect of net new loans and deposits over the next quarter. Ask these questions:

• Based on those projections, is there a funding gap?

• Do you have enough liquidity within the balance sheet? Or do you need to raise more?

• How much cash flow is the bond portfolio expected to return this quarter?

• On the funding side, does your bank have wholesale maturities that need to roll over?

These are all important questions that affect overall ALCO strategy. But begin with a strong understanding of your liquidity position.

Also ask, how does the cash flow forecast look over the next 12-24 months? And be sure you have a baseline forecast that will serve as the basis for stress testing.

Yes, you should be stress testing

You may find it difficult to look out past the next quarter of projected cash flows, let alone 24 months. Yet contingency planning and stress testing are integral pieces of the liquidity puzzle.

Forward-looking cash flow scenarios should be analyzed not only to show how liquidity could be stressed if you were to lose access to various funding resources, but also how the position could be impacted to the extent that loan demand accelerates while retail deposits disintermediate. Consider other economic scenarios or institution-specific events that may impact liquidity levels as well.

These “stressful” scenarios should all be compared to the bank’s current policy, and relief scenarios should be developed, for instances, where policy levels are breached. It’s essential to understand what type of liquidity event(s) it would take to push your institution into crisis-mode and the possible plans of action to counteract.

The other element of contingency planning is an effective risk monitoring system. A dashboard, or scorecard, mechanism should be in place to act as an early warning indicator for various quantitative and qualitative metrics that may indicate potential liquidity issues down the road.

A risk monitor report, in conjunction with ample stress-testing, forms the foundation of effective contingency liquidity planning that will complement your ongoing operational liquidity management process.

Communication is pivotal

All of the aforementioned liquidity management items need to be supported by effectively written policies and coordination with your board of directors:

• Overall liquidity strategy must be communicated between management and the board.

• Policy guidelines must be thoroughly planned and established.

• Everything must be well documented.

The ability for management to articulate the strategy, and how it interplays with asset and liability pricing, product, and growth decisions, is paramount.

About the author

Zach Zoia is a Consultant at Darling Consulting Group. He works directly with financial institutions throughout the country and across the ALM spectrum, with focus on interest rate risk modeling, liquidity management, capital planning, strategy development and regulatory compliance. He also leads new client model implementations and assists with executive education. In addition, he serves as Product Manager of Prepayments360°, DCG’s proprietary loan analytics tool.

Tagged under ALCO, Management, Financial Trends, Risk Management, Performance, Operational Risk, ALCO Beat, Feature, Feature3,